What was promising this year but was disappointed?

Written by: Zixi.eth

Continuing the article I wrote in December last year, we will open another article to summarize what happened in 2023 and look forward to the future in 2024. 2023 is a process of starting from low and moving high, with the secondary market continuing to rise. However, at the same time, the primary market continues to be deserted. It gives me the feeling that the primary market may be even more deserted than in 2022. This may come from:

- The primary market lags behind the secondary market by about half a year, and new entrepreneurs have not yet entered the market;

- Old entrepreneurs continue to pass away (they go to AI);

- There is an extreme lack of new stories. Most of the stories currently on the market are old stories.

The entire article is divided into three parts like last year, mainly explaining what was optimistic about this year but was disappointed, what is optimistic about next year, and what needs to be observed next year.

1. What was promising this year but was defeated?

1.1 Developer Tools-Everything in the world is beneficial

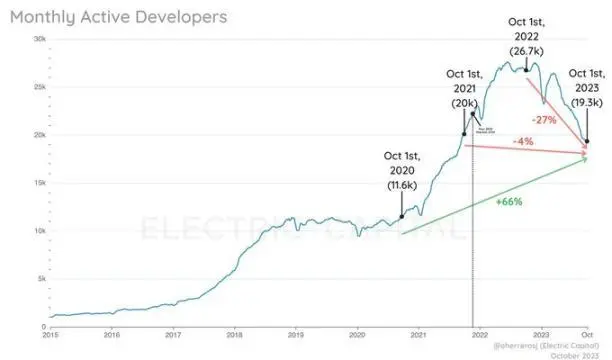

Compared to the same period in 2022, crypto MAD has fallen by 27% year-on-year, but thankfully, there is still a 66% increase compared to two years ago. Due to the decrease in new developers and the loss of old projects, the size of the developer tools market has declined to a certain extent this year. In addition, because the primary market for AI is so good in North America and China, many engineers have chosen to join the AI Nuggets.

Therefore, overall, the size of the developer tools market has declined to a certain extent this year. This is reflected in Alchemy’s primary and semi-market valuation - compared to the last round valuation of US$10.5 billion, the current valuation is only about US$3 billion. Consensys’ valuation of US$7 billion is now only around US$3 billion. But we are still confident in this market in 2024-2025.

We have also seen the growth of domestic developer tool data. For example, the number of developers on the Chainbase platform was 800 last year and increased to 6,000 in December this year. As the most directly beneficial track for developers to enter, if 24-25 is the next bull market, then the increase in the developer tools track will be very significant in 24-25. And I also believe that there will be a series of MA opportunities for developer tools in 24-25 years.

1.2 NFT—besides PFP, what else can it be?

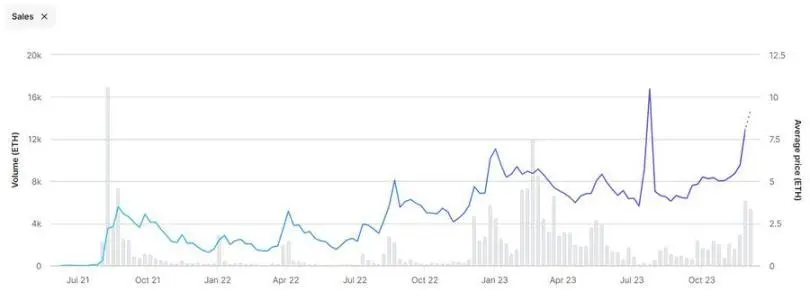

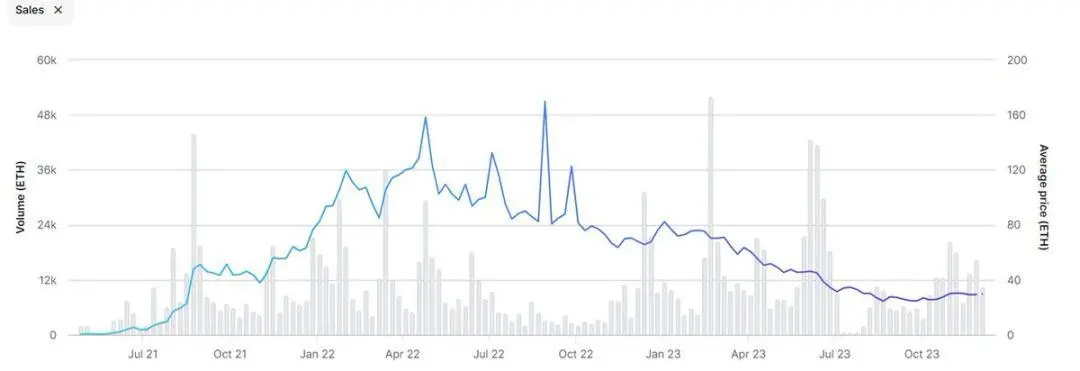

The traditional PFP story has made it difficult for everyone to pay for it. The picture below shows the price trend of BAYC in the past one or two years. In 2022, Yugalabs also launched a combination of APE + Monkey Land, which made the market fomo for a while. However, this year’s NFT market is very deserted, and it is difficult for large investors to pay tens of thousands or hundreds of thousands of dollars for NFT. In addition, Azuki has also given the market another chill. The AZuki Elemental launched this year is equivalent to directly copying and pasting one-click generation to start printing money. It is difficult to feel the team’s dedication.

However, it is worth noting that there are still some interesting projects emerging in the NFT market this year. For example, Little Penguin took the NFT+ offline toy route, which has indeed won unanimous praise from the North American market, allowing us to see a new route for pfp NFT.

Although NFT is on the decline in popularity this year, we have also seen uses of NFT other than PFP, such as the commercial value of entities + NFT (Li Ning/adidas + Monkey), brand pass cards (Starbucks), opera/concert ticketing, etc. NFT may gradually evolve into a “technology” in traditional industries next year.

2. What are you optimistic about next year?

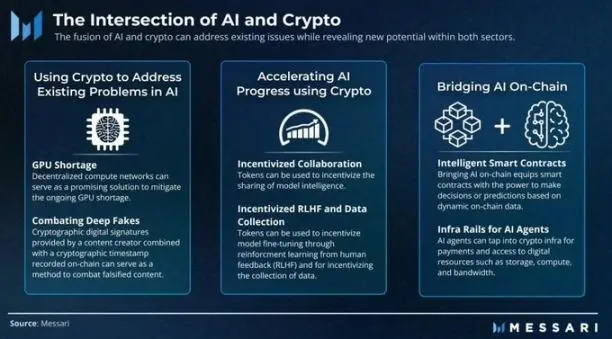

2.1 AI+Crypto——2B or 2C?

Let me make an interesting point first. If there is a bull market in 2024-2025, we will see a certain number of 2C game/social/C.AI/Chatbot web2 AI projects embark on the path of web3 currency issuance. This view comes from the fact that many 2C AI projects we have seen this year have relatively high homogeneity and relatively low income ceilings. Moreover, due to the increasing cost of computing power, it is difficult to even out the profit statement. After investing investors’ funds, exit channels should also be considered.

When income/game play/growth stagnates, actually issuing Utility tokens to increase game play is an idea that can be considered - on the one hand, issuing tokens to pull the market is a good mkt strategy, and secondly, it can also bring web2 users into the market (now wallet and account abstraction technology has developed well), so it may be a win-win approach for web2/3. In addition, this group of AI 2C entrepreneurs are also very young and have a high degree of acceptance of new things, which may also contribute to this.

Getting back to the topic, I simply divide crypto+AI into two categories: 2C and 2B. The 2C ones are similar to Myshell, NF, Worldcoin, etc., and the 2B ones are more, such as Modulus Labs, ChainML, EZKL, Questlab, , Gensyn, etc. I won’t go into details about 2C’s AI products. Whether they are games or similar products, they have been verified successfully in web2, and we have also seen it in web3.

The community of voice bots similar to Myshell is booming. Because Crypto+AI is still in its early days, it is still mainly 2B, such as serving project parties and providing them with on-chain agents; serving project parties and companies to do ZKML verification; serving LLM/Text to Video models or AI related companies, crowdsourcing data annotation, etc.

There is another interesting point about 2B AI companies, especially the data and computing power side, both are platform businesses - the upstream is the demand side of computing power/data annotation (such as various model companies), and the midstream is the computing power/data The marked distribution platform has various large, medium and small C downstream. The blockchain schedules long-tail retail investors downstream through a reward mechanism, but currently, data annotation scheduling is easier to implement, and the team has also received annotation orders from many large model companies. Scheduling computing power is difficult, especially when it comes to scheduling large-scale heterogeneous GPUs.

We have seen the vigorous growth of projects in many directions of 2B, and we are also looking forward to the performance of AI+Crypto in business and currency issuance next year.

2.2 Regulatory Compliance - Institutions Enter the Market

Regulatory compliance is an eternal theme. In fact, a large part of the increase at the end of this year comes from everyone’s pricein for Blackrock BTC ETF. The increase in the past month or so has been a good proof - “Just imagine what traditional funds can have.” If a part of it enters the market, there will be great growth."

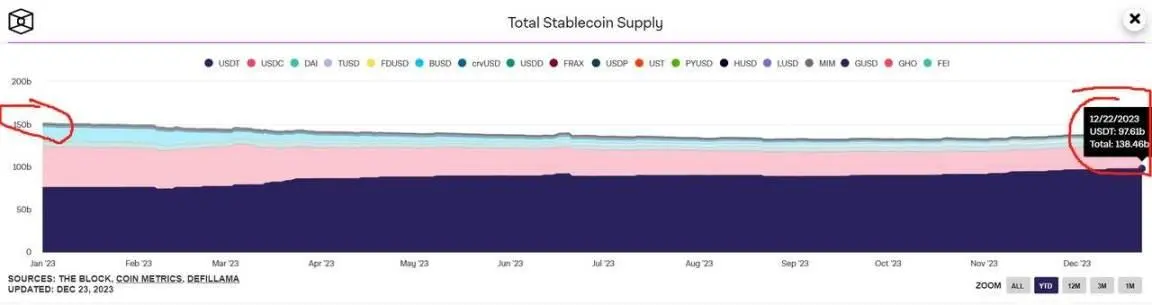

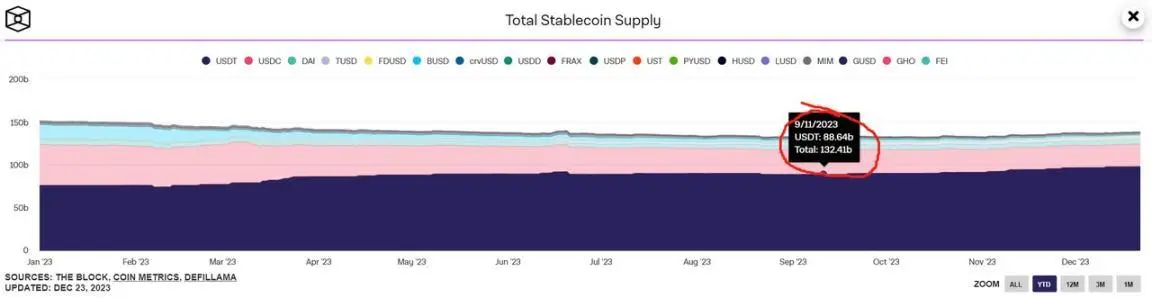

At the beginning of 2023, the market value of stablecoins was US$150 billion. September 23 was the lowest time for stablecoins in the past one or two years, with a market value of US$132.4 billion and nearly US$18 billion flowing out of the market. However, BTC has risen from US$17,000 to US$26,000, which means that mainstream funds have withdrawn, and the liquidity in the market has sucked blood from copycats to Bitcoin. However, from September to December this year, stablecoins only saw an inflow of 4 billion US dollars in 3 months, and BTC rose from 26,000 to 44,000.

We assume that not many traditional funds enter the market (after all, traditional funds think that the blockchain is a scam, and there is not much investment in the primary market), then this part of the money may be old people in the currency circle + traditional funds that know ETFs. Pull the plate. So once the BTC ETF is passed, the market will flow into the mainstream institutions with another 10 billion US dollars and 20 billion US dollars in one or two years. So how high can crypto rise? The analysis here will wait until the year-end summary in 2024 before reviewing it.

There are a few topics that I think are good regulatory compliance related:

- Stable currency 2. Exchange (Onchain/Offchain, especially for Perpetual) 3. Asset management. This part will not be described again.

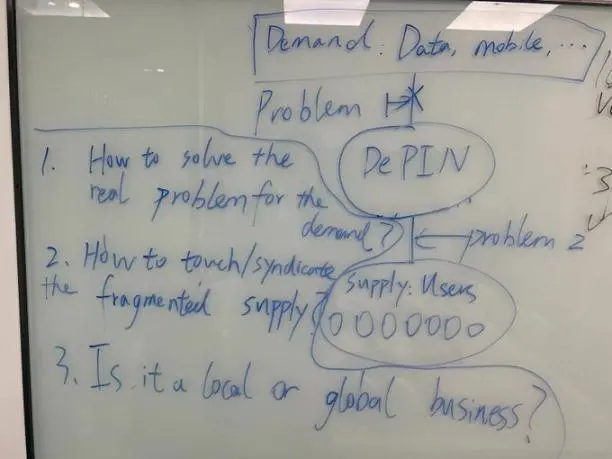

2.3 DePIN - How to use Crypto for distribution?

I have seen a lot of interesting projects recently, among which DePIN is the most interesting. It can be summarized as, XX+Crypto. XX is the main business, and Crypto is the distribution method. For example, Helium’s main business is Wifi, and Crypto/token is the distribution method; Hivemapper’s main business is that users feed map data to suppliers who need data, but uses Crypto for distribution; Questlab’s main business is to help with data The AI companies that are in demand do data annotation, but they just use Crypto to distribute it. Why use Crypto for distribution? I think this is the same logic as trading/coin speculation. Instead of directly telling users that they can make 100 yuan a year, it is better to give users a hope that they can make money. Moreover, using Token as a settlement method is more convenient than cash, especially in cross-border settlement for a wider range of users.

To complete a DePIN project, I divided it into three major questions.

The first big question is, what are the problems with the real demand in the upstream? For example, the real demand in Helium and Helium mobile is that communication data is expensive and the signal is not good. It costs a lot of money to lay out 4G5G base stations. There is no large centralized company in the United States that can do similar things, so we need decentralization. spread; data annotation is a real need of AI companies, and someone needs to help solve the problem of data annotation; rendering is a real need, so idle GPUs are needed for offline rendering; inference and training are also real AI needs, so it needs Idle computing power serves AI companies.

The second big question is how to access and synchronize these fragmented resources and connect them to the DePIN platform to serve the B-side. Quickly promoting the C-side was actually a difficult problem before. In traditional web2 businesses, such as e-commerce, community group buying, taxi-hailing, etc., the essence is to burn VC money to promote growth. But in Web3, it becomes ponzi to promote growth. The community relies on ponzi (actually burning the money of the people behind) instead of burning VC money to grow. This has been done in Axie/YGG/Stepn/Helium, etc. It is already a mature model in many cases.

In addition, for downstream contacts, the simpler the product, the easier it is to access it. For example, playing games online with GameFi, running Stepn, data annotation, installing a smart socket, etc. are all very simple things; but if you want to make a product that originally lives It will be relatively difficult to promote things that are not available in the Internet, such as installing a signal box at home.

Regarding how to syndicate downstream to connect upstream requirements, some are relatively simple to solve using scheduling methods, such as offline rendering, data annotation, bandwidth crawler, etc.; but there are some complex upstream requirements, such as heterogeneous GPU scheduling inference/training, etc. Very difficult to achieve.

The third big question is, is this a local or global business? There won’t be much explanation on this aspect. Global’s business will reach B and C faster, while Local’s business will reach slower. This is reflected in how many users and needs there will be in the end, as well as what the final project can achieve. How big.

3. What to observe next year?

3.1 GameFi√ / SocialFi?

First of all, you must understand the market value of Crypto and token. It is a good emotional amplifier and a good Mkt tool.

In 2022/2023, we have seen that there are very good teams in the East and the West making games. For example, the East has Funplus/Xterio, Matr1x, etc., and the West also has bigtime. Coupled with the sudden online game opinion draft on December 22, I believe this will (force) help Eastern game entrepreneurs to go overseas. This is a very big plus for Web3 Game. We look forward to seeing Axie/Stepn-like Eastern phenomenon-level game products again in 2024.

We have discussed before that social products may not be suitable for web3 because social networks have been very solidified in web2 and there is no need to reshape social relationships. But this year, a very good way to play is provided. Trading friends’ keys is actually no different from issuing inscriptions and assets in IEO (both are plates). We still hold a relatively conservative attitude when it comes to web3 social networking.

3.2 L2——Domestic and foreign troubles

The theme narrative of Infra in 2022 is Modular blockchain, and everyone is optimistic about the composability of ution, consensys, settlement and DA. And from 2020 to 2022, the technical barriers to L2 are indeed high, so the valuations of Arbitrum, Op and several major ZK projects are very high. I still remember that when analyzing L2 in 2021, we felt that the first-mover advantage of the ecosystem was very important with reference to the development of L1, so we will be optimistic about OP L2 first in 3-5 years, but we will still be optimistic about ZK L2 in the next few years due to technology iteration.

However, the iteration of technology seems to be far beyond our expectations. OP Stack can issue OP L2 with one click; now Rollup as a service company can even issue ZK L2 with one click. The composability is very high, so the barriers to L2 development are currently very low. In 2022, only 4 ZK L2s could be named. Now there are at least 10 ZK L2s on the market in 2023, and there are at least 5 more RAAS companies. The battle for L2 will be very fierce in 2024. Even Blur/Blast told VCs and retail investors that NFT Mktplace can not only vampire attack Opensea, but also attack other L2.

In addition, the EVM Competitors that are still alive now all have special skills, such as Tron for payments, BSC for games, and Solana for DePIN. In the future, how L2 will win the internal battle and how it will compete with EVM Competitor externally will be a very, very cruel battle. It may not be weaker than the Hundred Regiment War, the E-commerce War, and the Large Model War.

It is no longer 2020/2021, and the technical barriers to public chains have been much lower. In 2024, the environment is no longer dominated by public chains. Head DAPPs can choose top public chains at will, but it is difficult for top public chains to choose top DAPPs (unless they spend money). The current ecological path for public chain verification is: use your own strengths and take a path that others have never walked before. You cannot copycat. Only by leveraging your strengths can you win in differentiated competition.

3.3 Bitcoin Ecology - Is it a return of value or a bubble?

First of all, I very much agree with the view of a senior in Singapore: a 1% overflow of Bitcoin funds will create a huge ecosystem, and due to the lag of the Bitcoin network, the speed and effect of the fund overflow will be even greater.

In 2023, we will see the carnival of the Bitcoin ecosystem. The Bitcoin ecosystem has indeed gone through the four-year path of the Ethereum ecosystem in one year. But can we really create a unique ecosystem instead of replicating the old path of Ethereum (DeFi three-piece set + oracle + meme)? Institutions still need to be observed, but individuals can be shuttled.

This year the market is focusing on bottoming out. When token2049 ended in September this year, I felt that the industry was almost over. Especially after investing in ai+crypto, it was difficult to see meaningful new stories. However, the market picked up after October, and the increase convinced people and brought back everyone’s confidence.

In fact, if you think about it carefully, this market has already undergone too many iterations in 2022-2023. In the DeFi market, dex has gradually transitioned from spot to derivatives, and institutions are increasingly accepting DeFi; in the game market, developers from major web2 companies have already gone overseas. The basic research and development is completed and will be released in 2024; L2 has overcome many technical difficulties, and we can already issue OP and ZK L2 with one click; AI+Crypto also has many markets for it, such as data and computing power; social networking has also appeared; The Bitcoin ecosystem has also seen an influx of developers; Solana has been reborn, and depin has developed rapidly.

2024 may be even more exciting than the 2020/2021 bull market. I will continue to update next year’s article.