How will modularization, rollups, account abstraction, re-staking, etc. affect Ethereum?

Author: Christine Kim Galaxy Vice President of Research

Compiled by: Chief Villager of Ivory Mountain, Carbon Chain Value

Original title: “Ethereum Heavy Position”

Summary

The upcoming Ethereum Cancun/Deneb upgrade is expected to reduce the fees Rollup operators pay for block space, thus adversely affecting the revenue of Ethereum’s fee derivative protocols in the short term. ETH may underperform as a result, especially as Rollup projects built on Ethereum become increasingly interoperable with other settlement and data availability chains with stronger performance and relatively lower costs. In the long term, if the blockchain modularity theory proves correct, the main network fee driver for layer 1 public chains like Ethereum and Celestia will be the layer 2 rollup service providers, not the end users. Because of this, and the increasing adoption of account abstraction by second-tier public chains, the primary individuals holding Ethereum who pay for block space are expected to be rollup operators rather than end users.

Introduction

An age-old question in the cryptocurrency industry is how to scale public blockchains while maximizing (or at least maintaining) the network’s decentralization and security properties. The recent launch of Celestia represents the maturity of new solutions to the impossible triangle problem of public chain scaling. Celestia is the first highly optimized public chain to provide data availability (DA) for Rollup. As a data availability layer, Celestia has no native functionality for executing transactions. Instead, Celestia provides block space for Rollup to temporarily publish batches of user transaction data. As a DA layer, Celestia adopts strategies such as Data Availability Sampling (DAS) to reduce block space costs. These block spaces are dedicated to the execution layer, such as smart contract rollups that publish data on behalf of users on the chain.

Ethereum is also working to reduce the cost of block space for DA purposes, but at the cost of higher node requirements. Proto-Danksharding is a major code change for Ethereum’s next network upgrade. The upgrade, called Cancun/Deneb, is expected to increase the temporary data storage space of Ethereum nodes by 768kB. It is estimated that the additional block space used for rollup transactions will reduce Ethereum’s DA cost by at least 10 times.

The core of the modularity theory related to extended public chains is that the public chain should not have a single network to perform all core functions of general public chain computing (i.e., the overall or integrated blockchain theory), but should instead have responsibilities (such as execution or DA ) are outsourced to specialized infrastructure providers for enhanced functionality and performance.

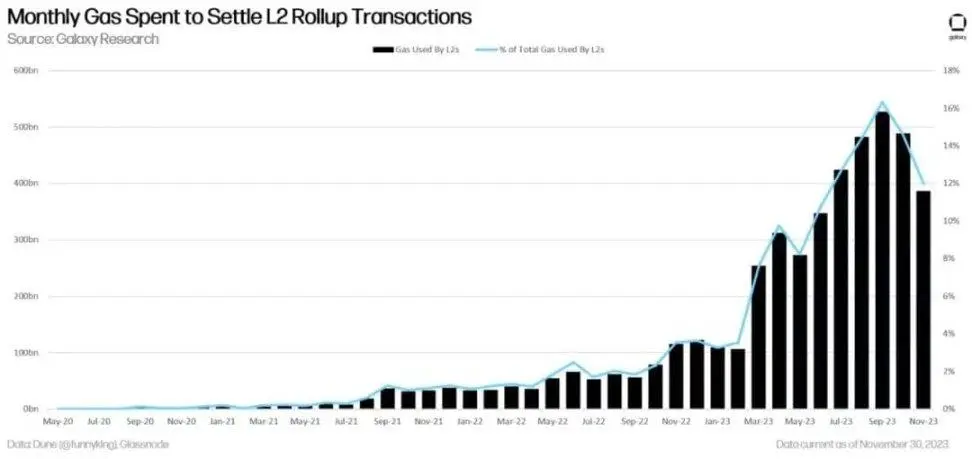

As Ethereum implements network upgrades to better support Layer 2 Rollups, the share of protocol revenue from Rollup Sequencers (i.e. entities that publish data from end users to the DA layer) is likely to be greater than direct L1 end users. Currently, Rollup accounts for 12% of all Gas paid on Ethereum, up from 3% at the beginning of the year.

Gas used to settle L2 Rollup transactions each month

This report will delve into the short-term and long-term prospects of value accumulation from L2 Rollup to L1 public chain, taking into account the impact of reset and account abstraction. The activation of recent upgrades such as Cancun/Deneb, coupled with the increasing flexibility of L2 to migrate away from using Ethereum as settlement and DA layer, may have a negative impact on the value of Ethereum in the short term, but in the long term as With the maturity of Rollup technology and the improvement of Ethereum’s DA function, the value of Ethereum will perform well.

This report is an extension of our previous report on Blockchain Modularity Theory, “The Significance of Blockchain Modularity,” which introduced many terms and concepts related to modularity theory and examined the costs of hierarchical blockchains. Generation and revenue drivers provide additional insights – which we recommend reading as a precursor to the discussion in this report.

L2 adoption in 2023

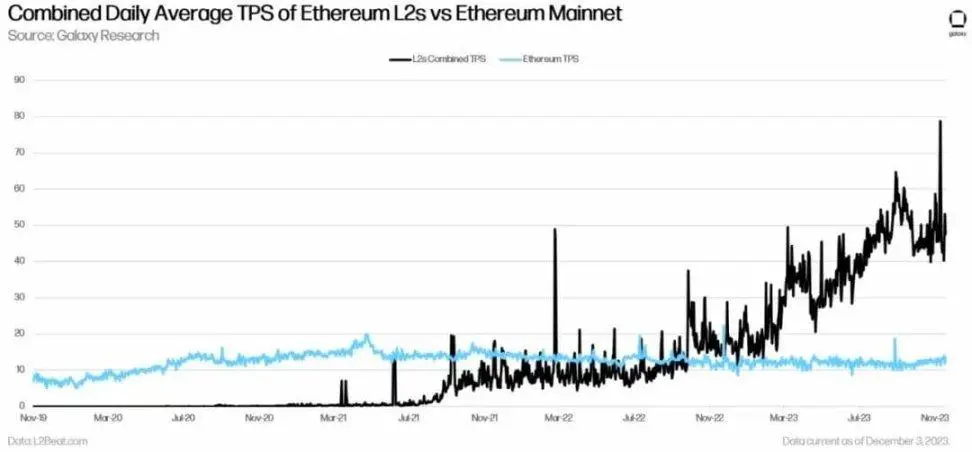

Ethereum L2 transaction activity has more than tripled since January. In 2023, L2 will have the highest nominal and percentage growth in total daily transactions.

The sum of daily average TPS of Ethereum L2s and Ethereum mainnet

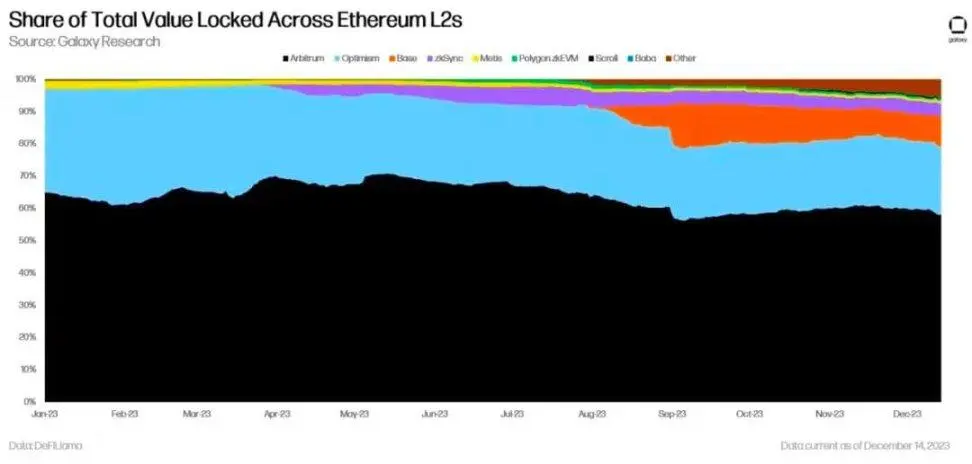

Within L2, Optimism and Arbitrum will see the largest declines in their share of total value locked in Ethereum L2 in 2023, down 11% and 7% respectively. Base and zkSyncEra experienced the largest value growth, with their share of total value locked in L2 increasing by 9% and 4% respectively. (Note: The total value locked metric is based on the USD value of the token and does not necessarily represent changes in the nominal value of tokens deposited into the protocol.)

Share of total value locked in Ethereum L2

It is worth noting that the Rollup called Base launched by the cryptocurrency exchange Coinbase this year has rapidly increased its adoption and popularity among L2 users. As of December 12, Base’s total value locked (TVL) ranked third in L2. In terms of trading activity, Base’s daily trading volume is sometimes higher than the two most widely used L2s (in terms of TVL) on Ethereum, Arbitrum and Optimism.

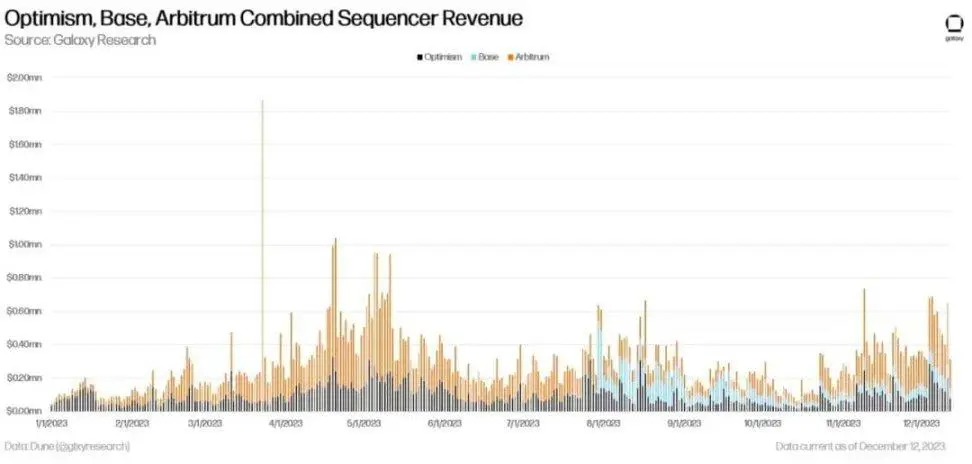

Among the top three L2s in Ethereum TVL, Base Sequencer generates approximately 20% of total revenue by sequencing user transactions and converting them into blocks in batches. To date, the Optimism, Base and Arbitrum sequencers have generated $140 million in revenue from user fees.

Optimism, Base and Arbitrum Combination Sorter Revenue

Looking forward to 2024, with the activation of the Cancun/Deneb upgrade, the cost of batching user transactions and completing transactions on Ethereum will be significantly reduced, thereby increasing the profit margin of Rollup sequencers while reducing Ethereum’s fee income.

Cancun/Deneb (Cancun upgrade)

The major code change in the Cancun/Deneb upgrade is Ethereum Improvement Proposal (EIP) 4844, also known as Proto-danksharding. Native Proto-danksharding creates dedicated block space for Rollup transactions. These transactions, known as “blobs,” will be priced based on a fee market independent of regular user transactions, and transaction data will only be temporarily stored for about three weeks. By activating EIP 4844, each block will add 768 KB of data space for rollup transactions.

The Cancun/Deneb upgrade will likely reduce Ethereum’s fee revenue in the short term, as EIP 4844 will reduce the block space fees Rollup pays Ethereum by more than 10x. Additionally, since Rollup technology has always had technical challenges in terms of lack of scalability, decentralization, and interoperability, the majority of Ethereum’s fee revenue will likely continue to come from end-users executing transactions directly on Ethereum, rather than L2. Until Rollup technology matures, Ethereum revenue is unlikely to benefit significantly from EIP 4844.

Short-term technical challenges

Here’s a closer look at three key areas of development that Rollup operators are prioritizing in 2023 and continuing to advance in 2024:

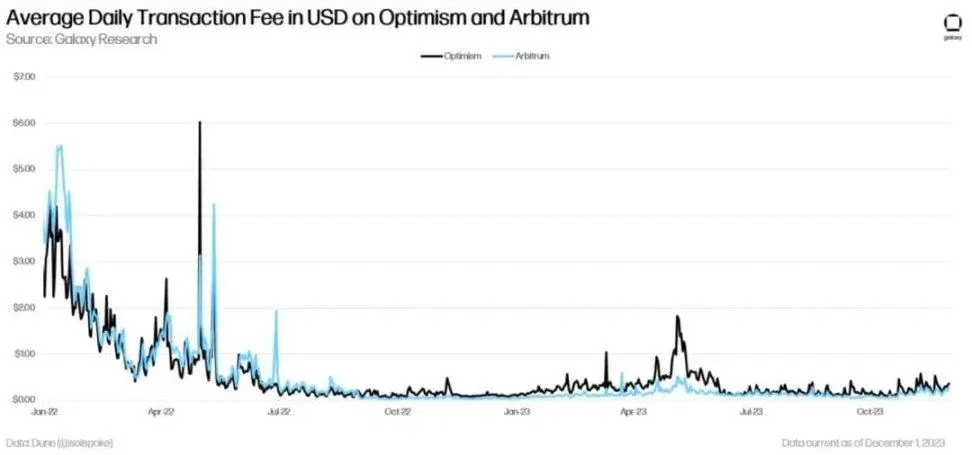

Scalability: Rollup is not immune to fee fluctuations. As we have highlighted in previous reports on blockchain modularity, in June 2022, when Project Galxe’s Arbitrum Odyssey marketing initiative triggered a large amount of on-chain activity, transactions in Arbitrum (the leading rollup in total value locked on Ethereum) Fees were briefly higher than Ethereum. Since then, Arbitrum’s fees have dropped significantly, especially after the release of Nitro in August 2022.

The Bedrock upgrade completed by Optimism in June 2023 also aims to improve the scalability of the network and reduce gas fees. Rollup’s scalability is an active area of development that developers are focusing on improving.

Average daily trading fees for Optimism and Arbitrum (USD)

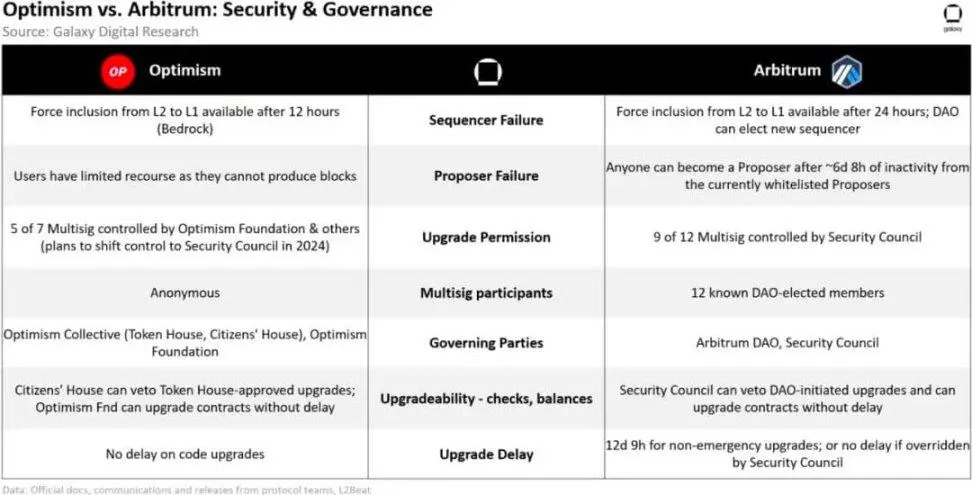

Decentralization and Security: Another area of Rollup development that developers are concerned about is decentralization. All cryptocurrencies on Ethereum are vulnerable to centralization attacks because they rely on a single node operator to sequence or sequence transactions and generate blocks. To increase decentralization and security, the cryptocurrency’s three core focus areas include (i) implementing validity/fraud proofs, (ii) expanding the set of operators for verification and ordering, and (iii) removing administrator privileges And assign Rollup control rights through governance.

Optimism & Arbitrum: Security and Governance

Interoperability: One of the main reasons why Ethereum occupies the general public chain market share is its strong network effect. As more users join Ethereum, the liquidity of the assets users interact with on Ethereum increases, and the value of the network increases in a positive feedback loop. This fragmented nature of liquidity is a barrier to Rollup adoption. The decentralized finance (DeFi) ecosystem benefits from the centralization of liquidity and the composability of Dapps on a single protocol. Therefore, solving the seamless migration of assets from L1 to L2, and seamless migration within the L2 ecosystem, is an important area of development that will help drive end-user migration from Ethereum to L2.

Advantages of Alternative DA Solutions

In the short term, Ethereum’s revenue will still be mainly generated by transactions initiated directly by end users on L1. As the cost savings of transacting on L2 increase due to L2’s scalability upgrades, and as Rollup’s decentralization and interoperability improve, user adoption of L2 will increase. Furthermore, cryptocurrency companies that choose to use alternative decentralized layers like Celestia to increase cost-efficiency can achieve higher profits simply by passing on some of the cost savings to cryptocurrency users. In addition to Ethereum and Celestia, other L1-level public chains such as NEAR have also announced their intention to shift to providing better services for Rollup as the DA layer.

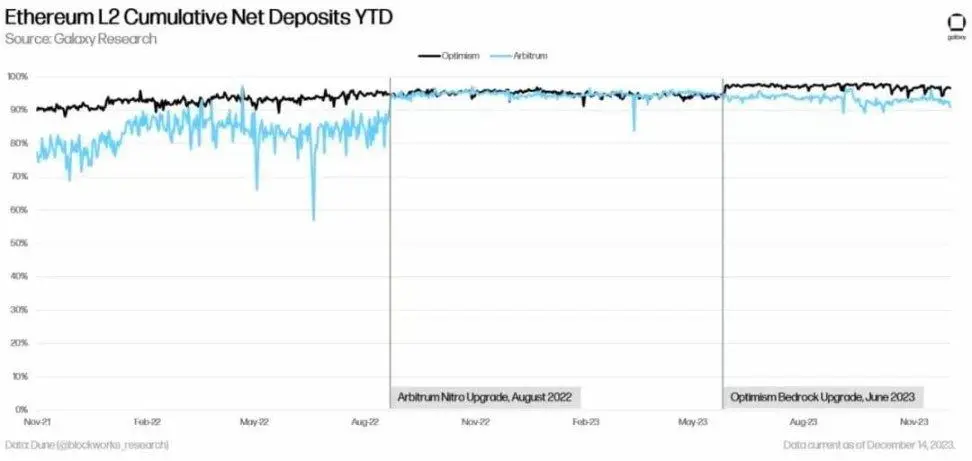

As shown in the figure below, users on L2 can spend more than 90% less transaction fees than users on Ethereum:

Cumulative net deposits on Ethereum L2 year to date

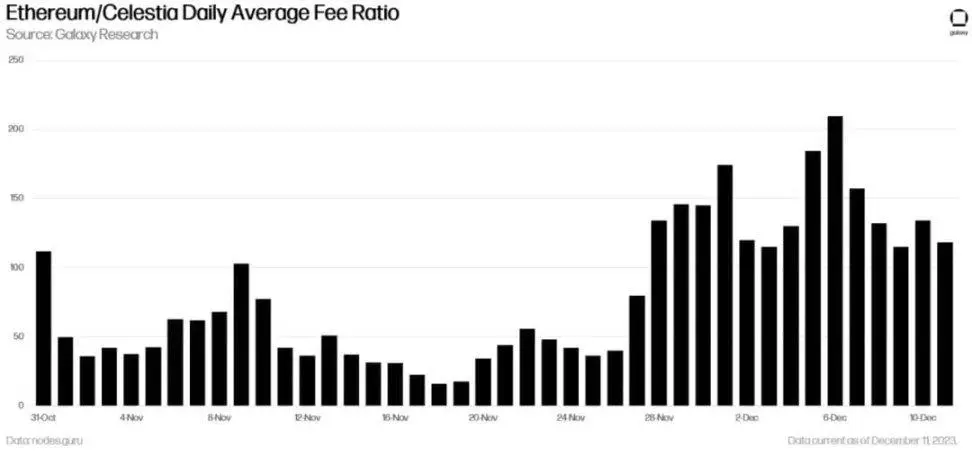

By publishing user transaction data on Rollup to Celestia instead of Ethereum, Rollup operators can achieve higher profit margins due to lower transaction fees on Celestia. On average, the handling fees on Celestia are several times lower than the handling fees on Ethereum, but this is largely due to the earlier birth of the Celestia public chain, which was launched on the mainnet on October 31, 2023. . The chart below depicts the fee ratio between Celestia and Ethereum, based on each protocol’s average daily transaction fees in USD. Celestia daily transaction fees are on average 80 times cheaper than Ethereum. (Note: The data below shows all types of user transaction fees on Celestia and Ethereum, not just transaction fees paid by Rollup orderers).

Ethereum vs. Celestia Daily Average Fee Ratio

As a new public chain that has been online for less than two months, Celestia has not been widely used for DA by L2 like Ethereum. Most of the trading activities on Celestia are not confirmations of Blob transactions, but activities related to the pledge and pledge delegation of Celestia’s native assets. As Blob trading activity increases on Celestia, transaction fees may fluctuate and trend upward. However, since Celestia has optimizations for DA that currently do not exist on Ethereum, it is unlikely that rollup fees on Celestia will be higher than on Ethereum, other things being equal.

In summary, we expect that as the cost of block space on Ethereum decreases with the launch of the Cancun/Deneb upgrade in 2024, Ethereum network revenue will decline, or at least be lower than it would have been without the Cancun/Deneb upgrade. Additionally, due to ongoing challenges with Rollup’s scalability, decentralization, and interoperability, it is expected that the majority of Ethereum network revenue will still come from end users rather than L2. Finally, if sequencers do not pass on all crypto cost savings to paying crypto users, but instead switch to other Rollup solutions such as Celestia, Rollup’s profit margins are expected to increase in the short term.

Long-term outlook

In the long term of five years or more, Ethereum’s revenue is likely to rise as blockchain-based applications and services see mass adoption, and rollup usage for transaction execution will be 10 times or even higher than that of Ethereum. higher. Cheaper L2 fees can bring new use cases to blockchain applications in gaming, social media, entertainment, sports and other industries. New use cases driving wider adoption of blockchain-based applications, also known as decentralized applications (Dapps), are expected to increase overall demand for Ethereum block space, thereby increasing Ethereum’s overall revenue. In this case, Ethereum’s main source of revenue comes from the Rollup service as the settlement and DA layer. Additionally, Rollup sequencers’ profit margins are tightening as competition for end-user activity intensifies.

In the coming years, the existence of multiple highly optimized DA layers may accelerate the migration of Ethereum L2 from publishing data exclusively to Ethereum to other DA layers that provide cheaper block space. These new DA layers may eventually challenge Ethereum more directly, which may undermine Ethereum’s current position as the most widely used rollup base layer. However, as discussed in the previous section, network effects are important, and Rollrp developers are working hard to improve interoperability and composability between Dapps launched on different Rollup protocols. To ensure that users and their liquidity can easily switch between different DA layers in the future, projects such as Caldera, Hyperlane, and Polymer are building tools to enable the Rollup protocol to run smoothly on multiple DA layers without affecting the user experience. . As long as shared settlement and DA layers like Ethereum provide advantages in terms of user experience and allow users to migrate assets between different rollups and Dapps running on these rollups, then Ethereum will likely continue to be the most valuable DA layer dominates.

Ethereum’s competitive advantages

Although Ethereum dominates the market in 2023 and is the settlement and DA public chain with the highest security, value, decentralization and network effects, there are still many public chains from Celestia and other public chains that have been specifically designed to support Rollup activities from the beginning. Competition will become increasingly fierce. Although Celestia has a smaller number and has just started to develop compared to Ethereum, it is possible that Ethereum’s dominant position as a DA public chain supporting Rollup transactions will be weakened over time, although this possibility is still very high. Small. To this end, Ethereum core developers are working hard to launch an upgraded version of Cancun/Deneb to enhance Ethereum’s DA functionality. However, when discussing the long-term impact of second-layer rollups on Ethereum revenue, one must consider the scenario that rollups will never be able to provide users with the same level of decentralization, security, and interoperability as the base layer.

Despite the advantage of lower fees, splitting application layer liquidity through L2 Rollups will likely anchor the majority of user trading activity to Ethereum in the short and long term. In this case, even if Celestia outperforms Ethereum as a DA layer, Ethereum’s competitive advantage as the world’s most decentralized general-purpose public chain may continue to win out and attract new users. Until then, Ethereum’s revenue will continue to be extremely volatile and dependent on the number of users interacting with applications directly on its base layer. Some users may perform transactions on Ethereum to take advantage of the network’s unparalleled decentralization and security as a general-purpose public chain compared to cheaper L2 and alternative L1.

As mentioned previously, in the short term, most end-user activity remaining on Ethereum rather than migrating to L2 will result in high fees and a temporary surge in network revenue. However, without scalability, Ethereum’s revenue will still be limited by limited transaction throughput and will remain unpredictable due to a lack of sufficient block space to meet new demand. The short-term revenue generated by user fees will eventually be dragged down by the network’s inability to support larger-scale user activities, which will adversely affect the long-term value of Ethereum as a general public chain.

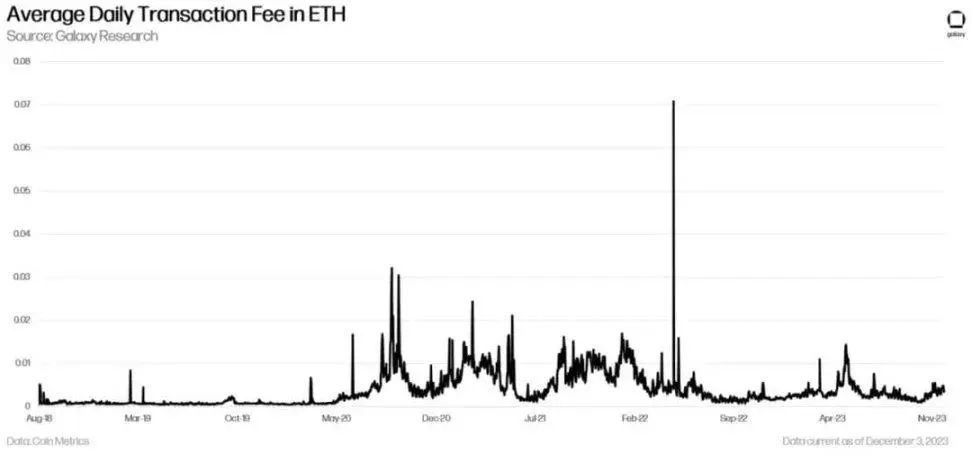

The following figure describes the fluctuations of Ethereum’s average daily transaction fees in ETH:

Average daily transaction fees in ETH

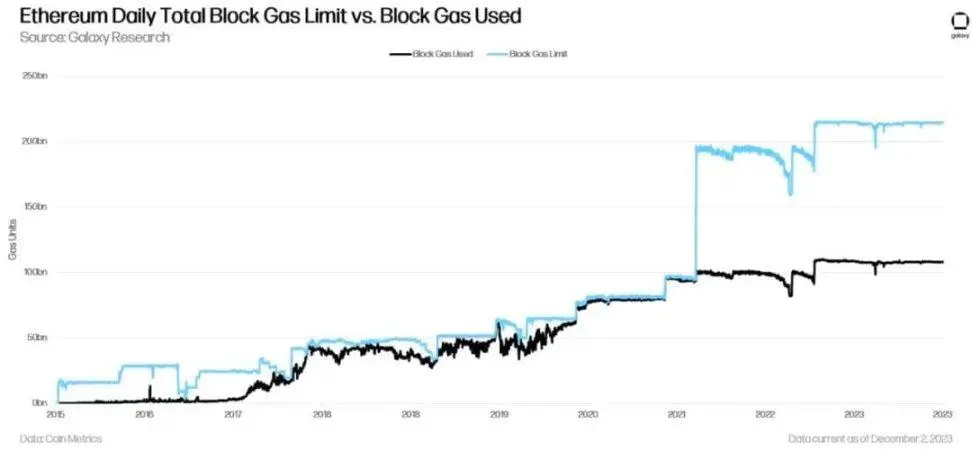

In the first six years of Ethereum’s existence, miners, the producers of Ethereum’s blocks, voted collectively to increase the block gas limit, effectively increasing the number of transactions that could be accommodated in a single block by at least 12 times. In August 2021, Ethereum core developers performed a hard fork (a backwards-incompatible network-wide upgrade) to increase the maximum block gas limit from 15 million times to 30 million times and transform the fee market to reduce Fees fluctuate.

The following chart illustrates how the Ethereum block gas limit has increased since Ethereum’s inception due to overwhelming user demand for block space:

Ethereum daily total block space limit vs. used block space

Despite these changes to Ethereum’s block gas limits over the years, fee volatility and limited network scalability remain a persistent issue that will be needed if Rollup proves unable to effectively inherit a large portion of end-user activity over the long term. A long-term solution.

Other considerations

Regarding the long-term value accumulation from L2 to L1, there are two other factors worthy of discussion, namely the trend of activating native account abstraction on L2 and the re-staking solution on Ethereum.

Account Abstraction

If the L2Rollup sequencer eventually becomes an intermediary service provider that end users rely on to interact with applications based on the public chain, rather than interacting directly with Ethereum, then in the future, users are likely to no longer directly hold Ethereum, but can Transaction fees are paid in stablecoins or even fiat currencies, depending on the design of the sequencer and Rollup, and the Rollup sequencer then converts these payments to Ethereum on behalf of the user to cover Ethereum transaction fees.

Increased flexibility and programmability in how fees are paid on L2 is primarily achieved through a technology called “account abstraction” which has not yet been implemented on Ethereum and may not be implemented in the near future . While account abstraction brings many benefits to the user experience, there is a lack of coordination among Ethereum core developers to prioritize the implementation of this technology ahead of other more pressing code changes, including increasing the maximum valid balance of validators, Verkle trees, Ethereum Virtual Machine object format, proposer builder separation, and more.

While there is a proposal to implement account abstraction without changing the core Ethereum protocol (ERC 4337), this proposal is unlikely to gain widespread adoption as it relies on Dapp developers updating their smart contracts, and end users choosing to use alternatives. memory pool. On the other hand, as an emerging technology, Rollups are the perfect proving ground for native account abstraction at the protocol level. Currently, Rollups such as zkSync and Starkware already do this, which means that end-user accounts created on these protocols automatically have enhanced programmability and usability.

The native account abstraction on Rollups will change the user experience when users interact with Dapps, because the account abstraction unlocks multiple new features for user transactions, including but not limited to:

Improve user experience for repeated or frequent transactions: For some on-chain games and DeFi applications, users need to submit multiple transactions. AC can be programmed to automatically allow transactions with certain Dapps, so users can avoid using private keys to repeatedly authorize interactions with the same smart contract.

The ability to stop the flow of assets in the event of a hack: If a user’s account exceeds a certain withdrawal limit, there may be embedded logic to stop the flow of funds.

Support for social recovery private keys: User accounts are also designed to rely on the user’s private keys and other social recovery devices to transfer funds. If a user loses their private key, the account can be programmed to regenerate a new key using two-thirds or three-fifths of the other social recovery devices.

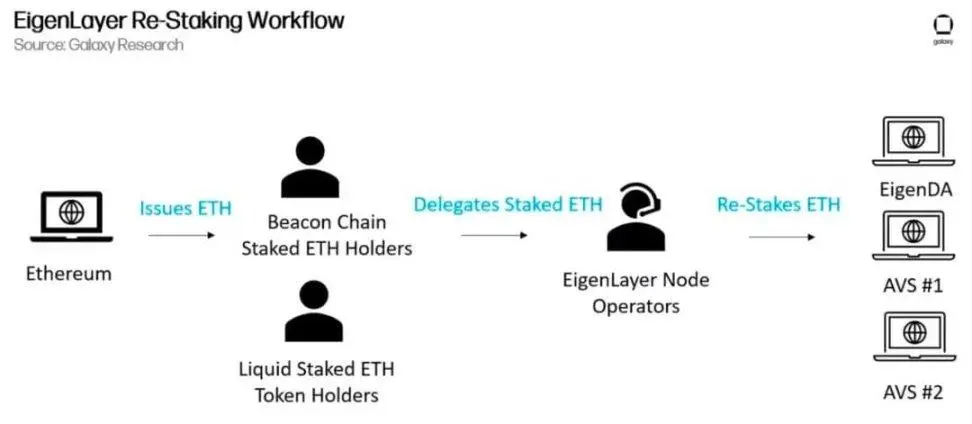

Re-Staking

Another consideration related to Ethereum’s rollup appreciation over the next five years is the maturation of rebooking protocols such as EigenLayer. As Galaxy Perspectives’ article on restaking explains, EigenLayer will enable end users to repurpose their staked ETH to secure other protocols and Dapps, thereby increasing yields. As of December 2023, EigenLayer developers are testing a restaking workflow for EigenDA, an additional DA layer secured by staked ETH to which the Rollup program will be able to publish data, rather than directly to Ethereum . Validator node operators who choose to re-stake via EigenLayer will be subject to additional cutback conditions (penalties) when validating transactions on Ethereum and EigenDA, but in return they will also receive benefits from both protocols instead of one. Earn higher returns from staking. The EigenLayer team expects to launch EigenDA on the mainnet in the first half of 2024. Thereafter, EigenLayer will join new protocols that validator node operators can re-stake outside of EigenDA.

EigenLayer re-staking workflow chart

It may take several years for a restaking protocol like EigenLayer to mature and gain widespread adoption on Ethereum. The first batch of Active Validation Services (AVS) on EigenLayer will be provided to node operators through re-staking, and these services will initially be carefully planned and tested in practice. EigenLayer developers intentionally limit the amount of ETH and liquid staking tokens that can be deposited into the protocol. Currently, the EigenLayer team has set the initial ETH deposit limit for EigenDA AVS liquidity re-pledge to 117,000 ETH. By December 18, 2023, this cap will increase to approximately 200,000 ETH. Additionally, on December 18, EigenLayer will begin accepting deposits from six new liquid staking tokens: osETH, swETH, oETH, EthX, WEBETH, and AnkrETH.

As of December 14, 2023, the amount of pledged ETH deposits for liquidity tokens including rETH, stETH, and cbETH, as well as native ETH tokens, accounted for less than 1% of the total Ethereum ETH deposits. Over time, the EigenLayer team will gradually increase the ability to deposit ETH to EigenDA and other AVS to ensure that the economic security of Ethereum and related AVS is not compromised until the protocol is fully tested. EigenLayer’s complete development roadmap will likely take several years, and there will be some unexpected bugs, especially as the AVS pool grows.

To the extent that re-staking becomes a reliable and scalable activity on Ethereum, similar to the liquidity staking activity that has become very common through the Lido protocol, then by repurposing staked Ethereum for operations such as sorting ) provides additional security that is expected to benefit Rollup. Additionally, Ethereum’s staking yield is expected to increase even as issuance by more validator node operators declines over time, which could increase demand for Ethereum beyond just Rollup orderers, Also includes DeFi applications and foundations. Even if ETH’s utility for executing transactions on Ethereum declines and Rollup adoption increases, re-staking activity may still be lucrative, which may encourage individuals and entities other than Rollup operators to purchase and stake ETH.

in conclusion

Ethereum’s revenue will benefit from being able to sustain larger transaction activity through L2, although in the short term, the network may face reduced revenue due to a lack of rollup adoption and the implementation of upgrades to subsidize rollup costs. Since the looming upgrade should reduce rather than increase fee payments, ETH is likely to underperform in the short term, at least to the extent that investors value Ethereum based on its fee-derived protocol revenue.

Rollup technology is an emerging technology that faces some technical challenges and application barriers in the short term. Over time, as Rollup technology improves in scalability, decentralization, security, and interoperability, much of the end-user activity will likely migrate from Ethereum to L2. When this happens, competition among L2s for users will intensify and rollup operators’ profit margins may decline.

In the long term, technologies such as native account abstraction on L2s will further reduce the need for end users to hold ETH directly. What is more likely is that as liquidity solutions exist and re-staking solutions like EigenLayer mature, end users and DeFi protocols will hold token representations of ETH and its accumulated returns. The main holders of native ETH are likely to be Rollup operators, who use the token to purchase block space on Ethereum on behalf of end users. Further research areas related to L1 value accumulation for L2 include: the impact of maximum extractable value on modular blockchain ecosystems, and the evolution of zero-knowledge proofs on Rollup design, its bridging, and economics.