Original by Zach Pandl, Grayscale

Original compilation: Felix, PANews

Points:

- ETH has risen well in 2023, but it is still behind Bitcoin and some other public chains. Grayscale believes that this can be attributed to the positive factors that have characterized Bitcoin this year, as well as the slow recovery of Ethereum on-chain activity.

- Although ETH has not risen as much as Bitcoin, ETH has outperformed traditional assets in absolute and risk-adjusted terms this year. Ethereum’s growing L2 ecosystem is likely to attract new users and support the Token’s valuation in 2024.

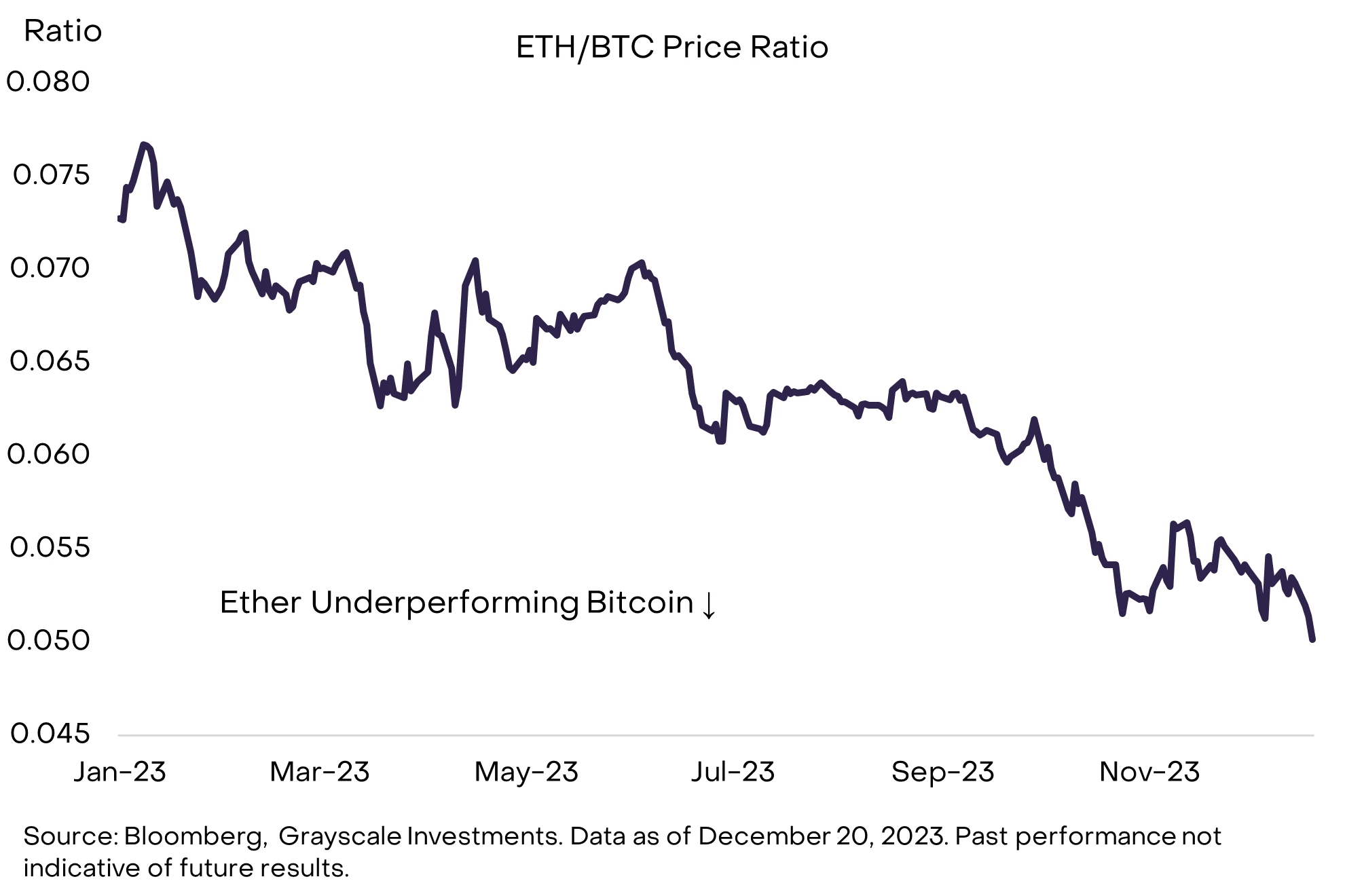

Few people say that an asset up 82% “underperforms,” but that’s what ETH is facing in 2023. The second-largest crypto asset has risen well this year (relatively low price Fluctuation) but is still well below BTC, which is expected to rise 162% this year. The ETH/BTC ratio declined throughout the year, reaching its lowest level since mid-2021 (Figure 1). Grayscale Research believes that ETH has performed “poorly” in 2023 for the following reasons.

Chart 1 : ETH/BTC ratio trending downward in 2023

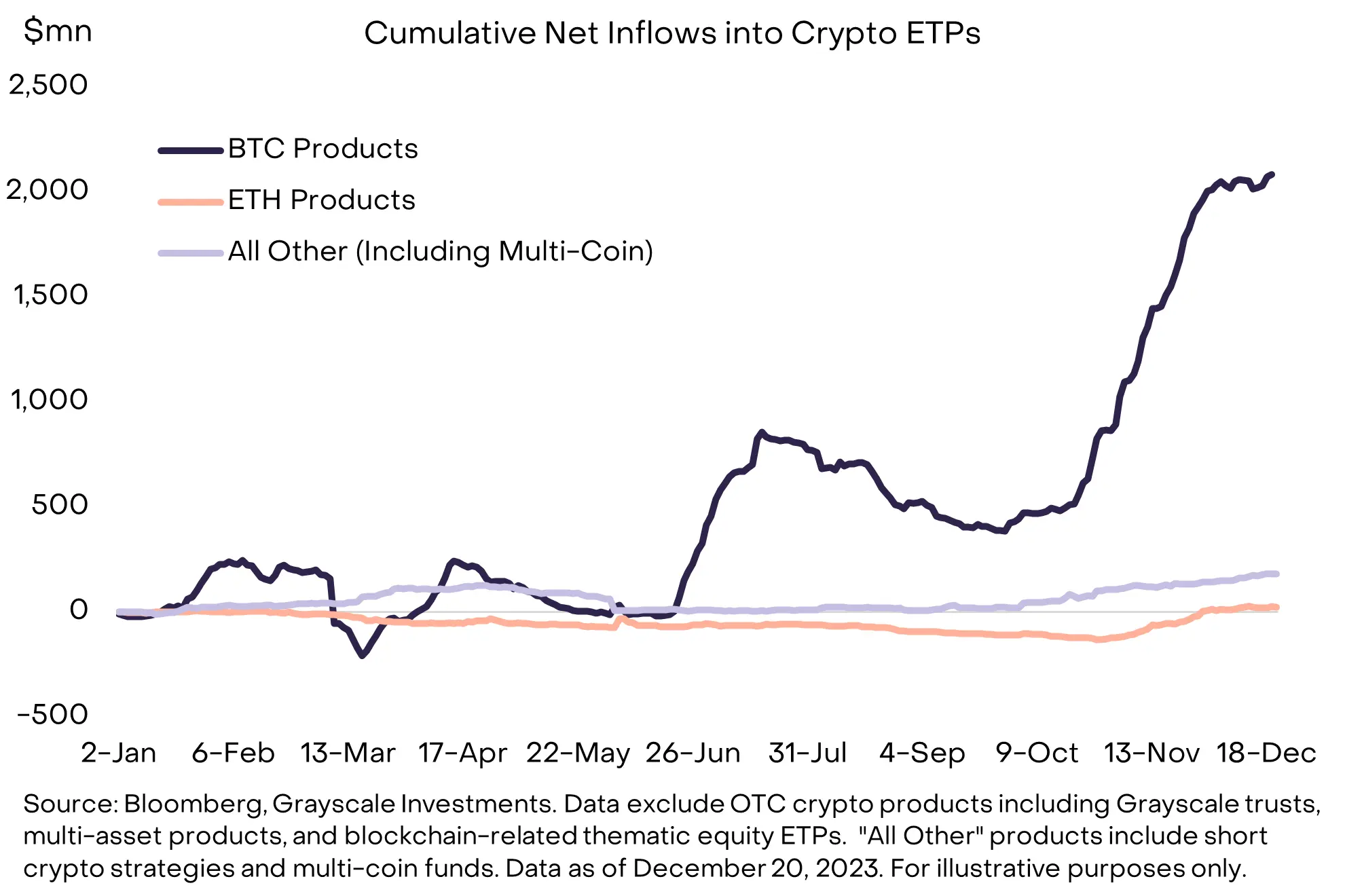

First, there are several Bitcoin-specific positives in 2023, including substantial progress in potential BitcoinSpot ETFs, and the instability of U.S. regional banks, highlighting the role of Bitcoin as an alternative to the traditional monetary system. These events appear to have driven inflows into Bitcoin-focused crypto investment products in 2023, making Bitcoin even higher this year. For example, Grayscale Research estimates that net inflows into Bitcoin-focused exchange-traded products (ETPs), including futures products in the U.S. and spot products overseas, will be around $2 billion in 2023. By comparison, net inflows into ETH-focused ETPs were just $24 million over the same period (Figure 2).

Chart 2: Bitcoin-specific positives appear to be driving more ETP inflows

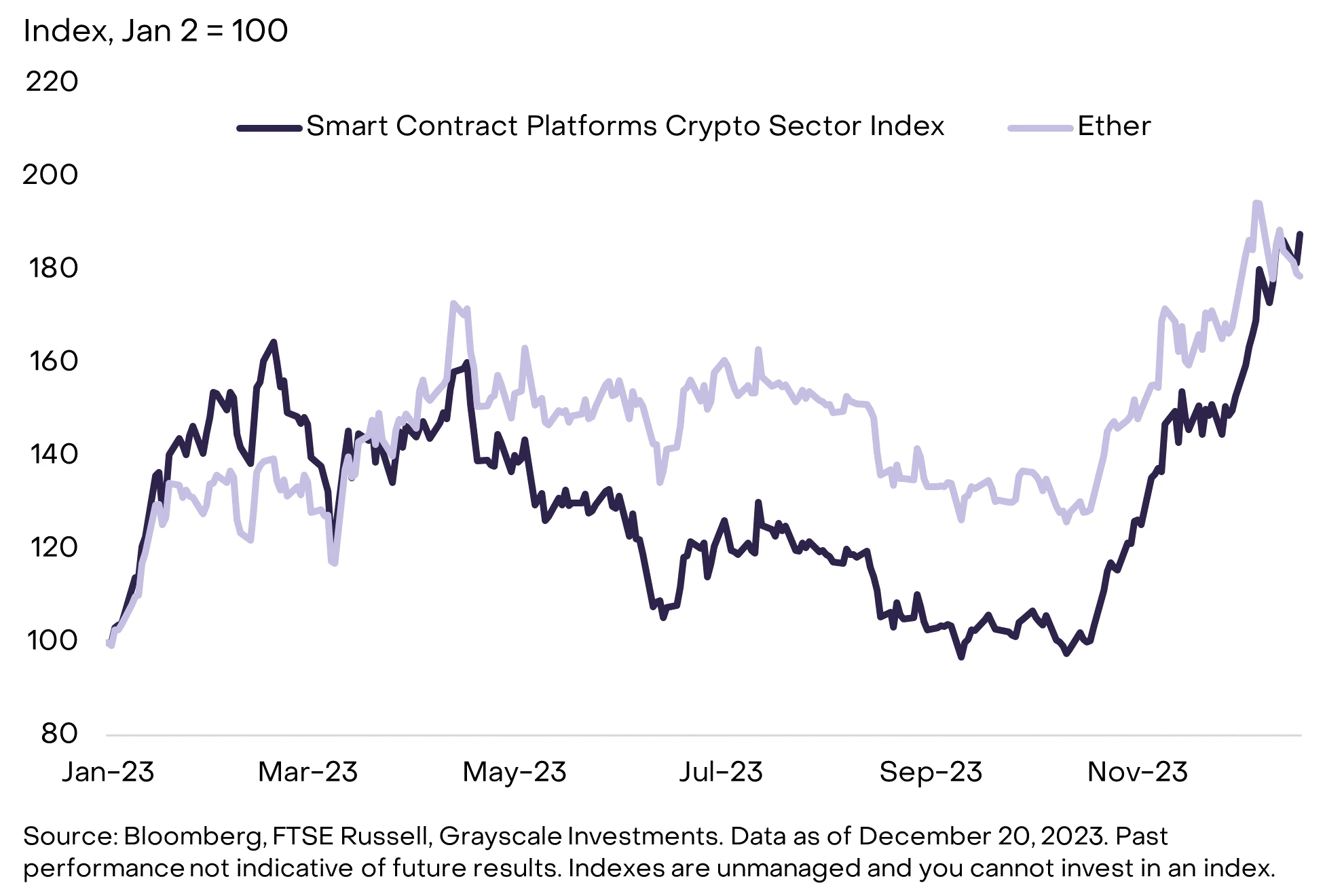

Second, most Smart Contract platform Tokens have risen less than Bitcoin this year, and ETH is largely consistent with that. As shown in Chart 3, the FTSE Grayscale Smart Contract Platform Crypto Industry Index rose by about 94% in 2023, only slightly above ETH. In the year ending October, ETH outperformed other Tokens, but other Tokens have also caught up recently (AVAX and SOL stand out). Throughout this year, ETH has performed near midstream among the 40 tokens in the Smart Contract Platform Crypto Industry Index.

Chart 3: Ethereum’s performance is in line with the Smart Contract Platform Crypto Industry Index

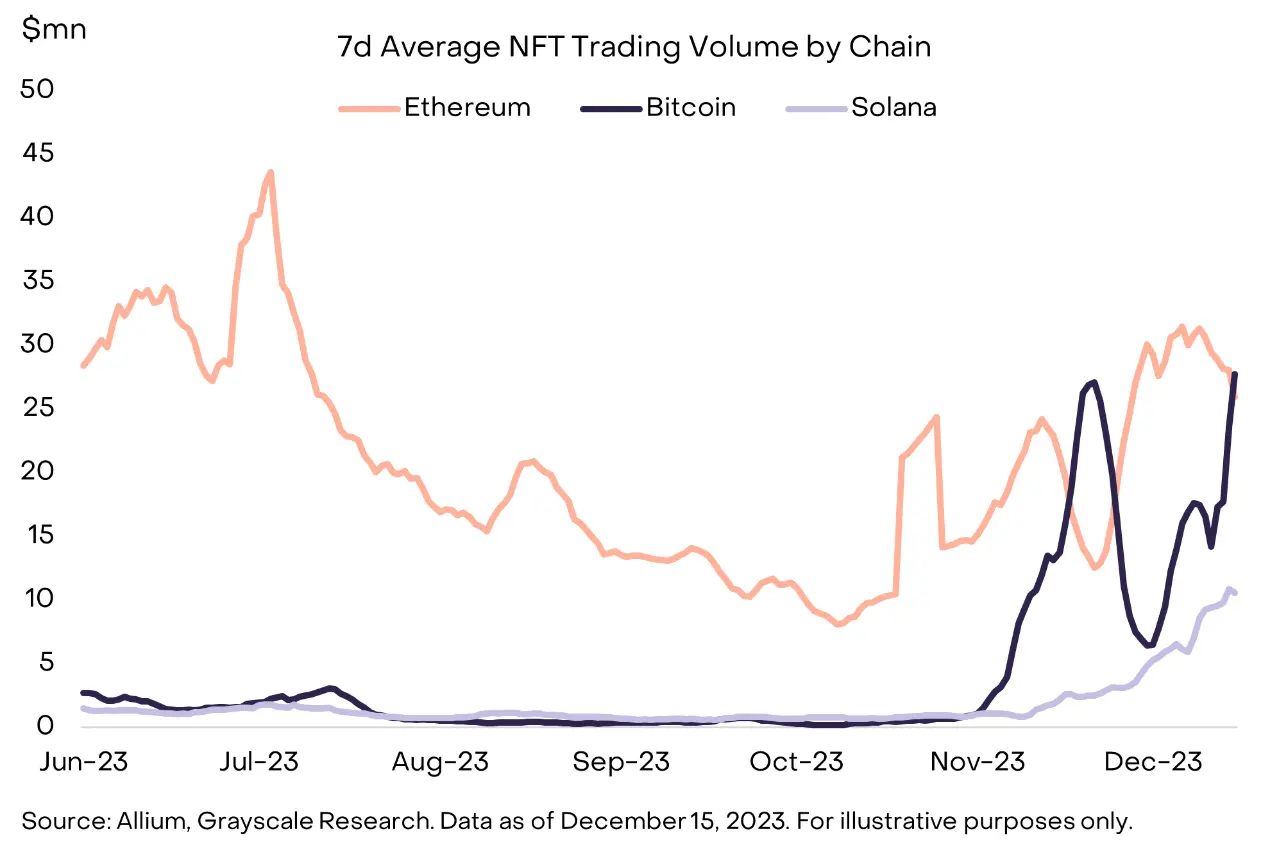

Third, on-chain activity (in some categories) of EthereumMainnet is slower to recover compared to other public chains. For example, since the start of the quarter, the Solana ecosystem Non-fungible Token trading volume has grown faster than the Ethereum ecosystem Non-fungible Token trading volume. Due to the rise of Ordinals, digital collectible transactions on Bitcoin have also increased significantly (Figure 4); in late December, the Bitcoin network’s daily Transaction Fee even surpassed Ethereum due to the large number of Ordinals transactions. Although Grayscale Research believes that Ethereum’s Non-fungible Token ecosystem remains constructive, the recent on-chain activity of the Solana and Bitcoin networks in this space has taken the majority of the market.

Exhibit 4: Non-fungible Token activity on Bitcoin and Solana chains is on the rise

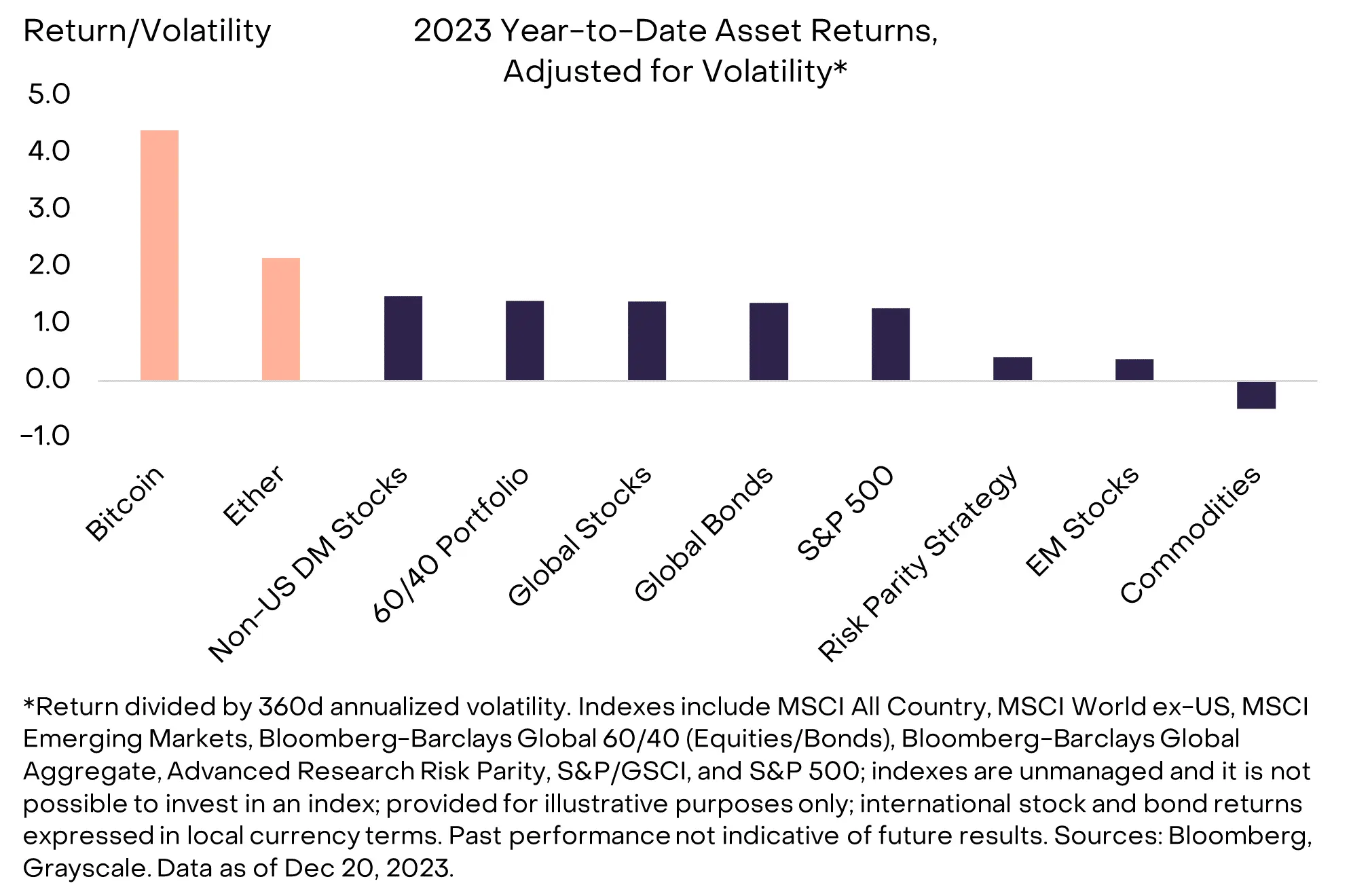

More broadly, while ETH has lagged Bitcoin and certain other crypto assets this year, ETH has significantly outperformed traditional assets in absolute terms and risk-adjusted returns (Table 5). Therefore, although the price of ETH has “only” increased by 82% this year, this rise should be seen as evidence of the crypto market’s ongoing recovery.

Chart 5: Risk-adjusted Ethereum outperforms traditional assets

While other Blockchains are in the spotlight in 2023, the future of Ethereum still looks bright. On top of that, Ethereum has historically benefited from the industry’s deepest network effects, with the most Decentralization Applications (DApps), the largest number of developers, and the highest revenue. Ethereum is pursuing a “modular” approach to development, where Layer 2 Blockchain ecosystem will be built on Layer 1 chains to allow for activity to scale. This work is still ongoing, and next year there should be an EIP-4844 upgrade that will drop the cost of Layer 2 scaling solutions to confirm transactions on Ethereum by a factor of 10-100. This will help dropEthereum Layer 2 the cost to the user.

If Ethereum can attract new users to its growing Layer 2 ecosystem, it could return to the center of the crypto scene in 2024. Therefore, the Smart Contract platform track may face the most fierce competition.

A low-cost “monolithic” Blockchain like Solana can provide a “silky” experience for new users, especially when combined with Wallets and other ecological dApps. In contrast, Ethereum’s modular environment can be more cumbersome to use, as users need to actively bridge assets between Mainnet and L2s. However, the development of these networks is still in its early stages, and it remains to be seen which Blockchain can design the most suitable product/market and accumulate the most value for their native Token over time. Once the end user has finished interacting with the application, the drawbacks of the current Ethereum user experience should be less severe, while other features of Ethereum, such as trusted decentralization, may attract developers and ultimately support Token valuation. For investors who are unsure of how the competition between smart contract platforms will develop, diversifying may be more worth exploring.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.