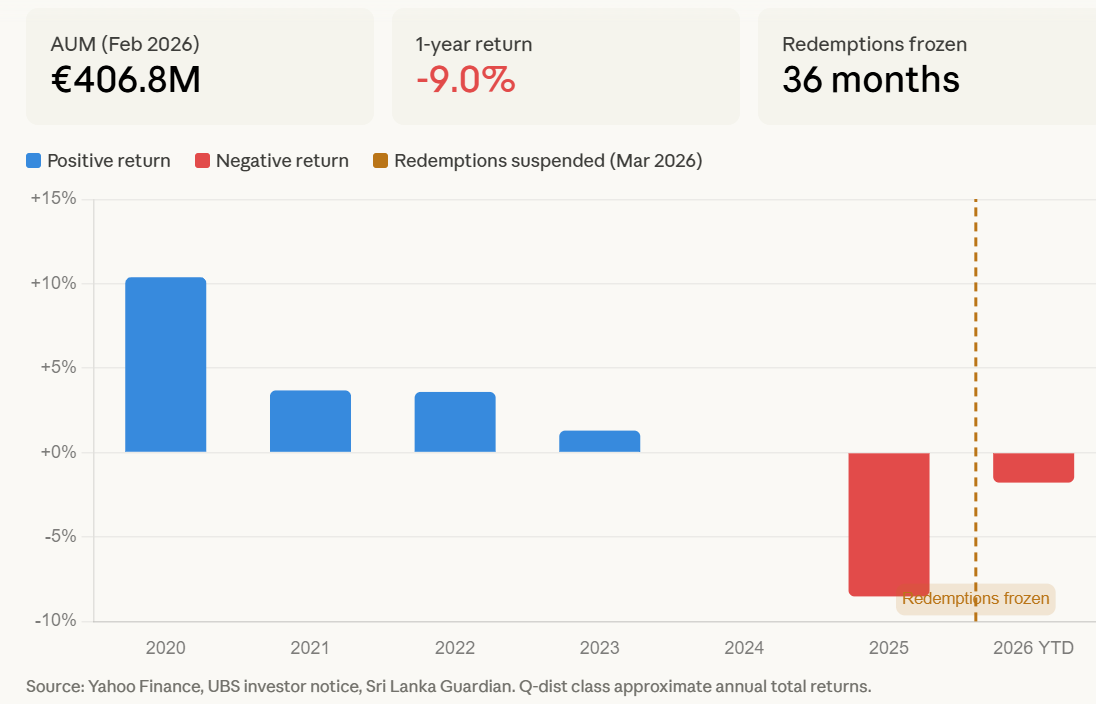

UBS’s German subsidiary, Union Bank for Real Estate Companies (UBS), announced via an investor notice on March 26 that its open-ended commercial real estate fund UBS (D) Euroinvest Immobilien has suspended all redemptions, with a maximum duration of 36 months. The fund’s assets under management are approximately $469 million. The statement said the fund’s liquid assets “are no longer sufficient to meet redemption needs and ensure proper management,” and that all redemption requests submitted after March 25 have been fully rejected.

Freeze Trigger Mechanism: A Double Hit of Valuation Declines and Redemption Pressure

(Source: BeInCrypto)

(Source: BeInCrypto)

The Euroinvest fund was launched in 1999, with a core strategy of investing in commercial real estate in major cities across Europe. Historically, it froze redemptions twice—during the 2008 financial crisis and again around 2014. This is the third time the fund has been frozen. The backdrop is a synchronized outbreak of multiple macro pressures.

Within the 12 months as of February 2026, the fund recorded cumulative losses of about 9% and its 2024 performance officially turned negative, as ECB rate hikes severely damaged commercial real estate valuations. The structural pressure factors driving this freeze are as follows:

Valuation side: Losses from a revaluation of European commercial real estate caused by rising interest rates, with the fund’s NAV continuing to shrink

Demand side: Escalating military actions by the United States and Israel against Iran have intensified market panic, leading to a surge in redemption requests

Expectation side: Market expectations that the ECB may raise rates as early as April have prompted investors to accelerate their exit from low-liquidity assets

Structure side: Open-ended funds hold real estate that has very low liquidity in units that can be redeemed immediately, creating an inherent mismatch between assets and liabilities

Celsius’s Mirror: A Structural Trap in Traditional Finance (TradFi)

There is a clear structural parallel between UBS Euroinvest’s predicament and the mechanism that dismantled the crypto lending platform. Both Celsius Network and Genesis Global accepted deposits with immediate redemption and allocated funds to on-chain agreements with very low liquidity. When withdrawal demand exceeded available liquidity, both collapsed in sequence.

UBS is facing the same structural trap; the difference is that the underlying illiquid assets are physical buildings rather than crypto tokens. In 2022, the crypto market paid a heavy price for liquidity mismatch; in 2026, this mechanism is repeating on a much larger scale in the traditional finance sector.

Broader Industry Contagion: UBS Is Not an Isolated Case

According to data from Nightingale Associates, under similar redemption pressure, Ares Management, Apollo Global Management, and BlackRock have recently either imposed redemption limits or adjusted withdrawal caps for their private credit funds. This shows that liquidity stress has spread from real estate to multiple categories of alternative assets.

Analysts noted that when TradFi platforms lock in exit mechanisms, institutional capital that might otherwise have flowed into risk assets such as Bitcoin (BTC) or Ethereum (ETH) could be trapped, further tightening overall market liquidity supply. Euroinvest’s freeze has been reported as the first major freeze event recorded by a European real estate fund since the recent escalation of Middle East geopolitical developments.

Frequently Asked Questions

Why did UBS freeze redemptions of the Euroinvest fund?

The fund claimed that its liquid assets were insufficient to meet the ongoing surge in redemption demand. The direct causes include falling valuations of European commercial real estate (about 9% losses over 12 months), upward pressure from interest rates, and redemption requests that erupted in a concentrated manner amid heightened geopolitical tensions—the triple factors together exhausted the fund’s available liquidity.

What is fundamentally similar between the Euroinvest freeze and the Celsius collapse?

Both face a structural mismatch between “open-ended redemption promises vs. very low liquidity of underlying assets.” Celsius’s underlying consists of crypto agreement positions, while UBS’s underlying is physical real estate. When redemption demand exceeds available liquidity, both mechanisms lead to a forced suspension of withdrawals, triggering a crisis of trust.

What specific impact does this freeze have on fund holders?

All redemption requests submitted after March 25 were rejected in full, and the maximum lock-up period is 36 months. At the same time, the fund stopped issuing new shares. During the freeze period, investors cannot exit or add to their holdings, and the fund shares they hold will temporarily lose all liquidity.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.