In traditional lending systems, capital providers and borrowers typically interact through multiple intermediaries, such as banks, credit platforms, or clearing institutions. While this structure is well established, it often results in longer financing cycles, higher costs, and limited cross-border accessibility. PACT addresses these issues by directly linking capital providers with borrowing institutions, allowing stablecoin capital to enter the global debt market more flexibly.

In practice, PACT does more than just facilitate lending. It also handles fund management, credit evaluation, repayment tracking, and risk control. This layered structure makes the lending process more transparent while improving visibility into credit risk, ultimately leading to better capital allocation.

At a high level, PACT’s workflow includes several stages: capital entry, credit assessment, loan issuance, fund utilization, and repayment. Each participant plays a specific role within these stages, forming a complete credit infrastructure that enables stablecoin capital to flow efficiently into real-world economic activity.

Overview of the PACT Credit Infrastructure

PACT is generally viewed as a stablecoin-based credit infrastructure whose core function is to connect global capital with borrowing demand. Unlike traditional lending platforms that focus on individual loan products, PACT provides the foundational structure that supports the broader credit market, allowing different institutions to conduct financing activities on top of it.

Within this framework, stablecoins serve as the primary source of capital, enabling fast cross-border transfers while reducing intermediary costs found in traditional finance. Through on-chain credit mechanisms, both loan data and fund flows can be tracked, significantly improving transparency. This transparency allows capital providers to better assess risk and supports the development of more efficient credit markets.

PACT’s infrastructure also accommodates a wide range of lending needs, including consumer loans, small and medium-sized enterprise financing, and asset management strategies. By connecting global capital with local lending markets, PACT directs funds to institutions with real financing needs, improving overall capital efficiency.

At the system level, PACT aims to build an open credit market that extends into areas underserved by traditional finance. This structure not only supports cross-border lending but also contributes to the broader digital transformation of global debt markets.

Capital Providers and Borrowers in PACT

Capital providers within the PACT ecosystem typically include stablecoin holders, asset management firms, and institutional investors. These participants supply stablecoin capital into the credit infrastructure, forming liquidity pools that fund lending activities. By participating, they indirectly support global credit markets while earning returns generated from lending operations.

Compared to traditional investment channels, this structure allows capital providers to engage more directly with credit markets. Instead of going through banks or funds, investors can allocate capital straight into lending opportunities, improving efficiency and reducing friction.

Borrowers, on the other hand, are usually fintech companies, lending platforms, or asset managers. These institutions often have strong access to local markets and lending demand but face limitations in cross-border financing within traditional systems. Through PACT, they can access stablecoin-based funding and deploy it into lending or asset management activities.

Once funding is secured, borrowers typically use it for consumer loans, SME financing, or similar credit operations. They then repay according to agreed terms, distributing returns back to capital providers. This creates a continuous capital cycle that sustains and expands the credit market.

How Stablecoin Capital Enters the PACT Market

Within the PACT protocol, stablecoin capital does not simply flow into a general pool. Instead, it enters the lending market through on-chain credit issuance and structured asset processes. By leveraging blockchain-native financial infrastructure, PACT allows capital providers to directly participate in financing real-world loan assets.

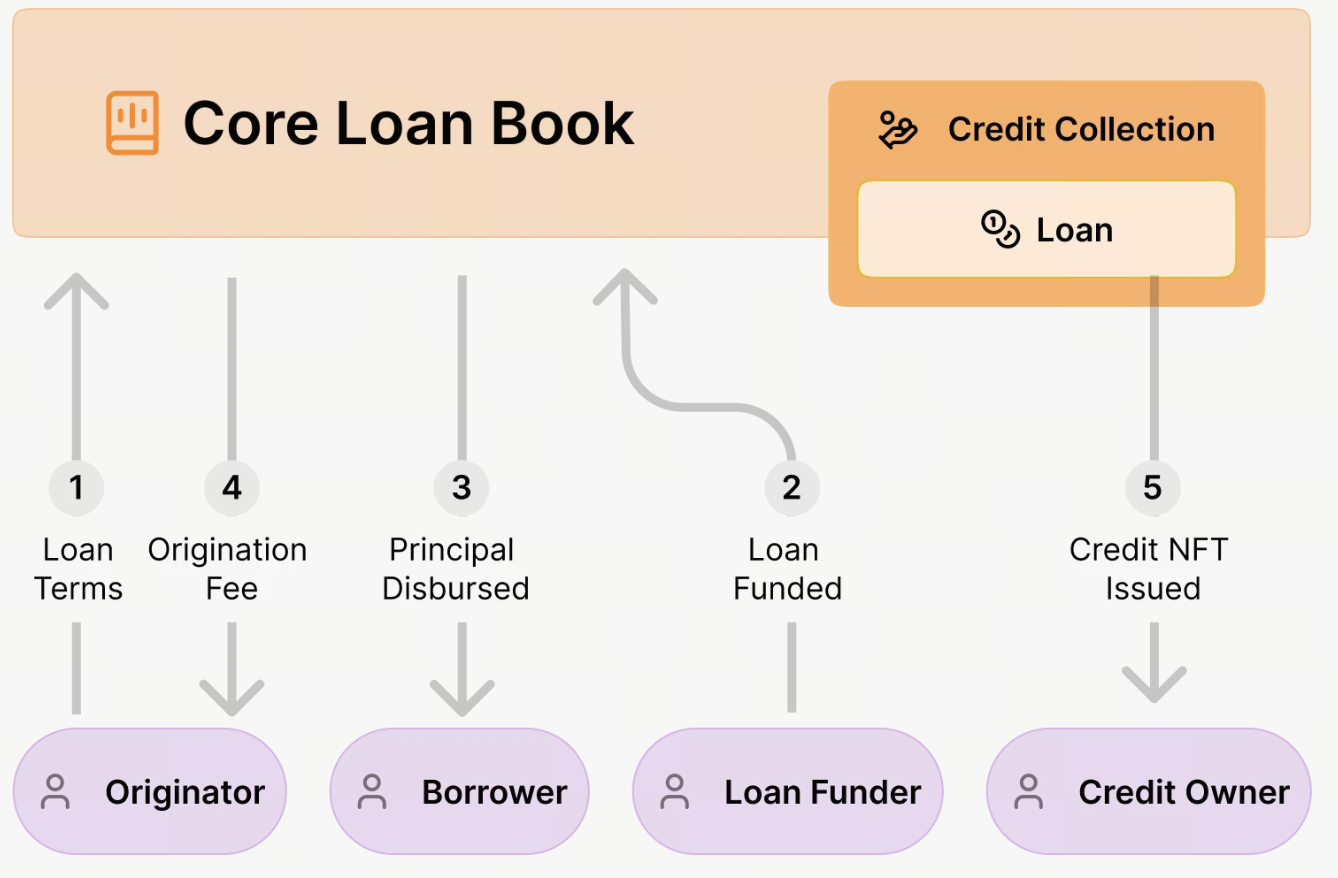

First, capital providers deposit stablecoins into the PACT protocol or associated liquidity pools. These funds are then used to support on-chain loan issuance. Unlike traditional platforms, PACT loans are created on-chain and governed by smart contracts that define key parameters such as principal, duration, interest rates, and risk scores.

Once funds are available, loan originators submit financing requests. These originators are typically fintech firms, lending institutions, or asset managers responsible for issuing loans in the real world, such as consumer or SME loans.

PACT then reviews the loan structure and generates on-chain loan assets. Each loan is typically tokenized as a Loan NFT, representing ownership and financial rights. This structure enhances transparency and allows capital providers to track loan performance.

After issuance, stablecoin funds are allocated to the borrower, who deploys the capital into lending or asset operations. Over the loan lifecycle, borrowers gradually repay principal and interest.

This approach allows stablecoin capital to flow directly into real financial markets while improving efficiency and risk management through on-chain transparency. By reducing intermediaries, PACT lowers costs and accelerates capital movement compared to traditional financing models.

PACT Lending Process Explained

Consider a fintech company in an emerging market looking to expand its small-scale consumer lending business. Through PACT, the company can access financing.

First, as a loan originator, the company creates a loan structure on the PACT platform, defining terms such as funding size, duration, and risk rating. Relevant credit data and documentation are uploaded and recorded on-chain to ensure transparency.

Next, investors provide funding in stablecoins. Once sufficient capital is committed, the loan is formally issued, and a corresponding Loan NFT is created to represent ownership.

The funds are then disbursed to the fintech company, which uses them to issue local loans, such as consumer credit or SME financing.

During the loan period, end borrowers repay principal and interest. These repayments flow back into the PACT protocol and are distributed according to predefined rules.

If the loan is part of a pooled structure, repayments may be distributed across different risk tranches. Senior investors typically receive returns first, while junior investors take on more risk in exchange for potentially higher yields.

This process forms a complete on-chain credit cycle, from capital provision to loan issuance and eventual repayment.

PACT Repayment Mechanism and Capital Flow

PACT’s repayment system operates through an on-chain loan management framework. Borrowers are required to follow a predefined repayment schedule, which includes principal, interest, and any applicable fees.

Repayments can be made in either fiat currency or stablecoins. Regardless of the method, all repayment data is recorded on-chain, ensuring transparency and traceability.

Once funds enter the system, they are automatically distributed based on predefined rules. For example:

-

A portion is allocated to principal repayment

-

A portion is distributed as investor returns

-

A portion covers platform or management fees

If the loan is part of a pooled structure, funds may also be distributed according to risk tranches. Senior investors are typically prioritized, while junior investors bear higher risk in exchange for higher potential returns.

PACT also provides real-time monitoring and repayment tracking. Loan performance data is continuously updated, allowing capital providers to assess risk and adjust strategies accordingly.

Once a loan is fully repaid, the associated Loan NFT is updated or closed, marking the end of its lifecycle. This completes the capital return and asset management cycle.

PACT Risk Management Structure

Because credit lending involves real-world assets and borrower risk, PACT employs a multi-layered risk management framework to reduce potential defaults.

First, it incorporates a credit evaluation mechanism. Loan originators must provide detailed data and risk assessments when submitting loan structures, enabling evaluation of loan quality.

Second, PACT supports pooled loan structures and asset diversification. Multiple loans can be bundled into a single pool, allowing investors to spread risk across different assets.

Additionally, PACT enables tranching. Loan pools can be divided into different risk layers, such as senior and junior tranches. This allows investors with varying risk appetites to participate while improving overall risk distribution.

PACT also offers real-time on-chain risk monitoring. Loan performance and repayment status are continuously updated, giving investors timely insights.

Finally, PACT uses a hybrid data model that combines on-chain and off-chain storage. Sensitive data is kept in encrypted off-chain databases, while verification data is recorded on-chain. This approach preserves privacy while maintaining transparency.

Through layered risk controls and on-chain visibility, PACT creates a more stable and reliable credit infrastructure for the stablecoin lending market.

Conclusion

PACT builds a stablecoin-based lending infrastructure through on-chain credit issuance and loan management systems. From capital entry to loan issuance and repayment, it establishes a complete on-chain credit market structure.

This model allows stablecoin capital to flow directly into real-world lending markets, supporting financing needs in emerging regions. At the same time, transparency and automated repayment mechanisms improve efficiency and risk management.

As on-chain credit and asset tokenization continue to evolve, PACT’s infrastructure may play a key role in connecting global capital with real-world lending markets.

FAQ

1. What are the main sources of funding for PACT?

PACT’s capital primarily comes from stablecoin investors, institutional funds, and asset management firms, all of which supply liquidity through on-chain loan structures.

2. How are loan assets managed in PACT?

PACT uses an on-chain loan management system, with Loan NFTs representing ownership and financial rights, ensuring transparent asset tracking.

3. How does PACT reduce lending risk?

PACT reduces risk through credit evaluation, asset diversification, tranching structures, and real-time on-chain monitoring.

4. How is PACT different from traditional lending platforms?

PACT leverages on-chain loan issuance and automated fund distribution to reduce intermediary costs and improve transparency, resulting in more efficient lending.