Forget the Rails. Own the Rider.

Note: 100% human-written. Typos and overthinking included.

Money is going through its internet moment.

The web already has its messaging (email), its publishing (blogs, social media), and its commerce (Stripe, Shopify). Now, it’s getting its financial system. Programmable by design, open by default, and borderless from day one. That system is being built on stablecoin rails.

But here’s the twist: even though the infrastructure is emerging, we still lack the crucial experience. And history tells us that’s where the biggest winners are crowned.

Infra enables. Experience wins.

Every cool tech shift starts with infrastructure. But no one remembers the protocol. What all remember is the product that made it usable.

In 1982, the Simple Mail Transfer Protocol (SMTP) made email possible. However, it wasn’t until 2004, when Gmail launched with a clean product, massive storage, and a functioning spam filter.

Search engines existed long before Google. AltaVista. Archie. Lycos. But Google simplified everything. It was faster. Cleaner. Smarter.

Skype didn’t invent the Voice over Internet Protocol (VoIP). WhatsApp didn’t invent messaging. But they made it work for people.

We’re at the same inflection point with money.

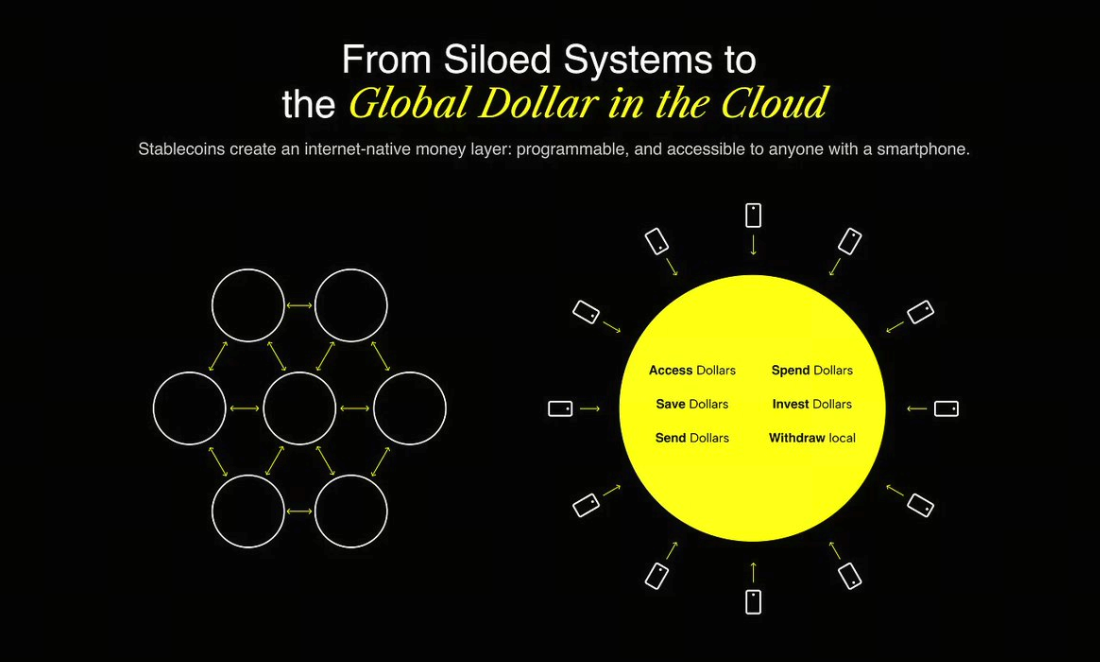

Stablecoins are helping to create an internet-native financial system.

And it’s not theoretical. It’s already working.

- In 2024, stablecoins settled over $15.6 trillion on-chain.

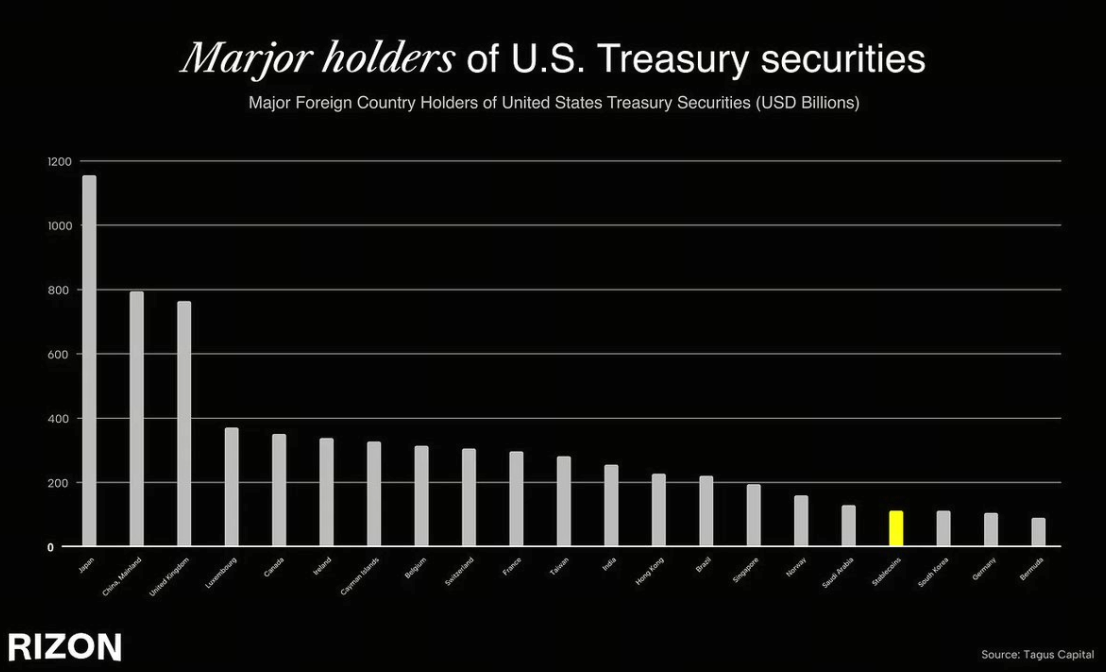

- Tether is now the 18th largest holder of Treasuries worldwide, ahead of countries like South Korea, the UAE, and even Germany. For perspective, the world’s fourth-largest economy now holds less U.S. debt than a stablecoin issuer.

- Yet despite this scale, stablecoins in circulation are just $263 billion, compared to $22 trillion in the U.S. M2 money supply -barely 1% penetration.

- Today, fewer than 5% of people globally use stablecoins, but adoption is projected to reach 7-10% within the next five years, unlocking massive new waves of financial inclusion.

- In regions like LATAM, MENA, and Southeast Asia, stablecoins already function as parallel dollar economies, where people rely on them daily to escape inflation, capital controls, or local banking failures

We’ve never seen financial infrastructure scale this quickly, especially not across borders. Stablecoins are already reaching millions of users globally. And for good reason: they’re fast, borderless, dollar-denominated, and run on open protocols. In a world where 1.4 billion people are underserved and even more are restricted by capital controls or volatile local currencies, stablecoins offer something revolutionary: a plug into the global dollar network, accessible from anywhere with a smartphone.

But here’s the problem: try using stablecoins today and you’ll quickly hit a wall. Spending is clunky. Onboarding is confusing. Everything is wrapped in jargon, wallets, gas fees, networks, bridges…

That’s the gap. We have a new monetary operating system — call it the Internet-Native Financial Cloud — but most people can’t access it.

It’s like getting a PS2 steering wheel for Christmas… but no PlayStation to plug it into (true story, btw). There’s a massive opportunity hiding in plain sight: Making this feel normal. Invisible. Smooth as butter. 🧈

Why UX is the moat

In fintech, owning the user means owning the relationship. That’s where trust is being built, behaviors are shaped, and long-term value is created.

While user experience is rarely the strongest argument when participating in strategic sessions— in fintech, it’s everything. Because this isn’t just software, it’s money. And money demands confidence.

Just look at the biggest success stories in neobanking- Revolut, Cash App, Nubank. These companies operate in different markets, but they all follow the same playbook: deliver a world-class user experience.

As stablecoins enter their next phase of adoption, the real winner will be the brand people trust when sending money to family, the card they instinctively use to pay for lunch, and the app that quietly replaces their local bank. It will be the experience that makes stablecoins invisible-and makes them feel like regular money. Regular, but global.

Why now?

What makes this moment so urgent and so exciting is the alignment of three forces:

1. The infra is ready

- Stablecoins are liquid and getting deeply integrated.

- Wallet-as-a-service platforms, such as Privy, and embedded on-ramps, like Bridge, technical UX hurdles solvable.

- Credit card issuance, compliance-as-a-service, and KYC providers-all are battle-tested.

2. Regulation is catching up

- Hong Kong launched stablecoin-specific legislation in 2024.

- The U.S. Treasury’s GENIUS Act outlines a future path to regulated, scalable stablecoin usage.

3. The user base is growing-fast

- In LATAM and Sub-Saharan Africa, stablecoins are already leapfrogging banks.

- 1.4 billion people globally remain underserved. But they own smartphones.

- Gen Z is default internet-finance-native.

This isn’t the speculative hype cycle. This is infrastructure maturing, regulation paving the way, and a massive consumer market waiting to be served. Billions of people still lack access to modern financial tools and services, yet they have smartphones, internet access, and a growing familiarity with stablecoins. The rails are finally here. Now it’s a race to build the experience layer that brings it all to life.

Global Finance Needs an Upgrade

That’s why we’re building Rizon — a neobank built from the ground up for the internet-native financial system.

Spend instantly, anywhere

- Get your virtual or physical card in minutes. Accepted at over 100M+ merchants worldwide.

Send money like a message

- Transfer dollars globally, instantly, and for free-no middlemen, no borders.

And the early signal is clear. Just 5 weeks after public launch, @getrizon"">@getrizon has already crossed 30,000+ installs across iOS and Android, averaging ~300% week-over-week growth across key metrics (like funded accounts and transacting users).

But that’s just the beginning. In the near future, we’ll layer in RizPoints, credit, yield, tokenized assets, and more. All on-chain. All under the hood. All invisible to the user. We’re not building a dashboard. We’re building your global money app. A Brand. A Statement.

The Stablecoin standard is being written now

We believe the most undervalued play in fintech right now is building a stablecoin experience that feels like Apple Pay. One that fades into the background. One that just works. One that wins by being obvious, trustworthy, and global. That’s exactly what we’re building.

And if we’re even half right about the size of this shift…

Let’s go.

Disclaimer:

- This article is reprinted from [isurvila]. All copyrights belong to the original author [isurvila]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

- Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

- Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.

Share

Content

Related Articles

The Future of Cross-Chain Bridges: Full-Chain Interoperability Becomes Inevitable, Liquidity Bridges Will Decline

Solana Need L2s And Appchains?

Sui: How are users leveraging its speed, security, & scalability?

Navigating the Zero Knowledge Landscape

What is Tronscan and How Can You Use it in 2025?